Watch

Watch Gamma is known as the second-order derivative after delta, which is the first-order derivative. Option Gamma is the delta of the delta. This means option gamma measures the rate of change in the delta to a change in the underlying price.

If the delta represents speed, option gamma is the acceleration. In the chapter on the delta, we had said that delta could be used for a small price move, but for a larger price move, gamma is to be examined. Delta is not linear and changes position as the price of the underlying changes.

For example, suppose the Nifty 17,700 call for August 2022 expiry is trading at Rs 195 with delta at 0.55 and gamma at 0.0008. If Nifty moves up by 100 points to 17,800, the 17,700 call would move by Rs 55.08 (100 x (0.55 + 0.0008)). The new option premium now would be in-the-money at Rs 250.08 (Rs 195 + Rs 55.08), and the new delta would be 0.5508. But, if the Nifty falls by 100 points to 17,600, the 17,700 call will fall by Rs 54.92 (-100 x (0.55-0.0008)). The option premium would now be Rs 140.08, and it would be out-of-the money; the new delta would be 0.5492.

For example, suppose the Nifty 17,700 call for August 2022 expiry is trading at Rs 195 with delta at 0.55 and gamma at 0.0008. If Nifty moves up by 100 points to 17,800, the 17,700 call would move by Rs 55.08 (100 x (0.55 + 0.0008)). The new option premium now would be in-the-money at Rs 250.08 (Rs 195 + Rs 55.08), and the new delta would be 0.5508. But, if the Nifty falls by 100 points to 17,600, the 17,700 call will fall by Rs 54.92 (-100 x (0.55-0.0008)). The option premium would now be Rs 140.08, and it would be out-of-the money; the new delta would be 0.5492.

Gamma helps traders’ who delta-hedge their positions as a high gamma value would significantly move the delta as the underlying moves, and vice-versa for a low gamma value. Also, it helps a normal trader understand the sensitivity of his profit and loss account on account of gamma.

Long gamma: Here the aim is to remain in-the-money

Gamma is a positive value for all options. A long gamma value is one where an option has a positive gamma exposure. This means gamma is added to the delta of an option with an increase in the price of the underlying and deducted from the delta of an option with a decrease in the price of the underlying. All long options have positive gamma. Long gamma essentially means accelerated changes in option prices when the price of the underlying moves up or down by 1 point. This will result in an accelerated profit for a long position or accelerated losses.

Positive gamma for a long call: Since long calls have a positive delta, if the price of the underlying increases, gamma is added to the delta to make it more positive and move towards +1 or move towards in-the-money. However, when the price of the underlying falls, gamma would be deducted from the call option delta, making it less positive and moving it towards zero or out-of-the-money.

| Long Gamma call | Points | Delta | Gamma | New delta |

| Increase in price | 1 | 0.55 | 0.01 | 0.56 |

| Decrease in price | 1 | 0.55 | 0.01 | 0.46 |

Positive gamma for a long put: Since long puts have a negative delta, if the price of the underlying falls, gamma is deducted from the delta to make it more negative and move towards -1, i.e., it would move towards in-the-money. However, when the price of the underlying increases, gamma is added to the put option delta making it less negative and moving it towards zero or towards out-of-the-money.

| Long Gamma call | Points | Delta | Gamma | New delta |

| Decrease in price | 1 | -0.55 | 0.01 | -0.56 |

| Increase in price | 1 | -0.55 | 0.01 | -0.46 |

Short gamma: Here the aim is to remain out-of-the-money

An option position with a negative gamma is known as a short gamma. This is the opposite of long gamma. This means gamma is deducted from the delta of an option with an increase in the price of the underlying and added to the delta of an option with a decrease in the price of the underlying. All short options have negative gamma. A higher gamma for an option seller increases the risk as the underlying can move up or down rapidly, causing losses.

In the case of a short call option: Since short calls have a negative delta, and if the price of the underlying falls, the gamma will be added to the call option delta making it less negative and moving towards zero or out-of-the-money. However, if the price of the underlying increases, then the gamma would be deducted from the delta, making it more negative and moving towards -1 or move towards in-the-money.

In the case of a short put option: Since short puts have a positive delta, and if the price of the underlying increases, gamma would be deducted from the delta making it less positive and moving towards zero or towards out-of-the-money. However, if the price of the underlying decreases, then gamma would be added to make it more positive and move it towards +1 or move towards in-the-money.

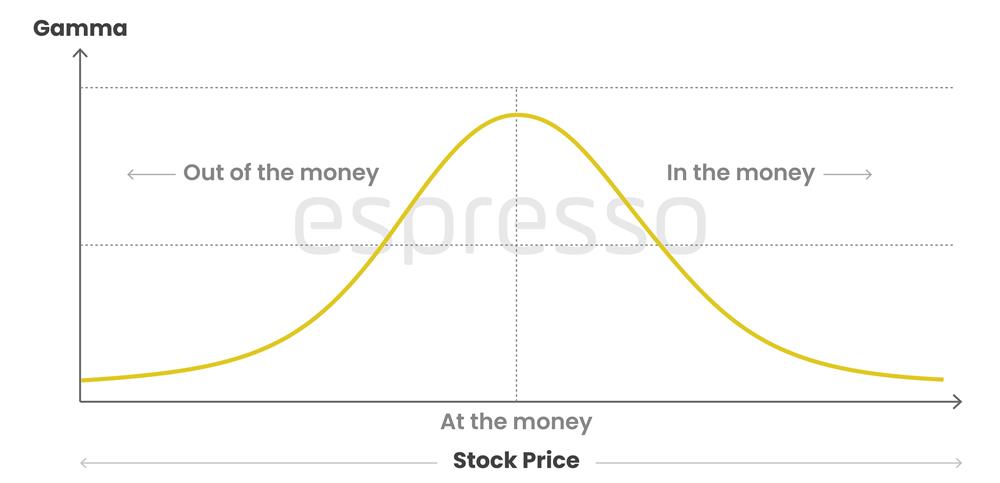

Moneyness

Gamma is at its peak when the option is at-the-money and tapers out on both sides (in-the-money and out-of-the money) and is similar to a bell curve. Since delta is 0.50, any small movement in the underlying can cause a substantial change in delta. The delta for an out-of-the-money option is near zero, and therefore, delta movement is insignificant. Deep-in-the-money options, which have a delta of +1 for calls and -1 for puts will not have any gamma impact as deep-in-the-money options behave like an underlying and have gamma close to zero.

Expiration

Gamma of at-the-money options rises as expiration draws closer, and the bell-curve gamma chart peaks more sharply. It should come as no surprise that options that are at-the-money and have a short period till expiration are the most unstable and have the highest gamma. On the other hand, when expiration draws near, gamma decreases for both in-the-money and out-of-the-money options. The bell curve is brought further nearer to zero at both ends.

Volatility

An increase in volatility causes the gamma of in-the-money and out-of-the-money options to increase, while the gamma of at-the-money options falls. While declining volatility increases the gamma of at-the-money options, the gamma of in-the-money and out-of-the-money options fall.

Conclusion

Gamma can be of little use in trades that involve plain buying and selling of options. However, gamma comes into play when complex strategies are involved. Delta and gamma relationships in complex strategies become much more important. If an overall position has a positive delta and positive gamma, the position becomes profitable as the prices go up. However, if the overall position has a positive delta but negative gamma, then the negative gamma would drag the delta towards zero and eventually make it negative, resulting in losses. Therefore, one has to be aware of when and where to book profits and exit the position.

Things to remember

- Gamma is of little use in trades that involve plain buying and selling of options. However, gamma is useful where complex strategies are involved.

- All long options have positive gamma.

- If an overall position has positive delta and positive gamma, the position becomes profitable as the prices rise. But, if the overall position has a positive delta but negative gamma, then the negative gamma would drag the delta towards zero, eventually making it negative, resulting in losses.

0

|

0

|

0

0