Watch

Watch Theta is the decline in the time value of an option. The value of an option consists of two parts — intrinsic value and extrinsic value. The intrinsic value is the difference between the option strike price and the current underlying value, while the extrinsic value is the difference between the option premium and the intrinsic value of the option. Extrinsic value is anything other than intrinsic value.

The extrinsic value consists of time value, volatility, interest rate and dividends, which are external variables that affect the option value. Theta represents the time value of an option that decays as the option approaches expiration. It is important to understand time value and time decay. Theta or time decay is represented in currency terms. For example, a theta value of -16 would mean the theta decay would be Rs 16 per day. Theta value is negative for an option buyer and positive for an option seller. Therefore, an option selling trade is known as a positive theta trade, and an option buying trade is known as a negative theta trade.

Time value, expiration & time decay

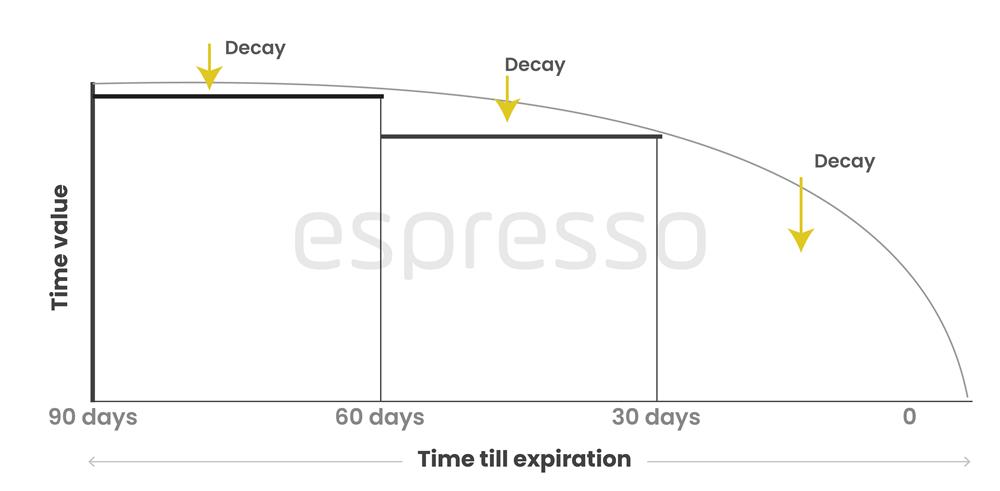

Time value is the willingness of the option buyer to pay over and above the intrinsic value. An option contract, in the beginning, has more time value with more time to expire. This is because the larger the time for expiration, the greater the probability for the option to expire in-the-money. Consequently, the larger the time value of the option. With more time in hand for expiry, the likelihood of the price movement increases. As the time to expiration contracts, the time value decreases. This is known as time decay or theta decay of an option. The most important thing to observe in theta or time decay is that it is not linear.

Time value is the willingness of the option buyer to pay over and above the intrinsic value. An option contract, in the beginning, has more time value with more time to expire. This is because the larger the time for expiration, the greater the probability for the option to expire in-the-money. Consequently, the larger the time value of the option. With more time in hand for expiry, the likelihood of the price movement increases. As the time to expiration contracts, the time value decreases. This is known as time decay or theta decay of an option. The most important thing to observe in theta or time decay is that it is not linear.

Theta decay accelerates as the time to expiration nears expiration except for deep out-of-the-money options. Time decay will be relatively less for a contract that has 60 days of expiration, but it will start decaying faster as it reaches 30 days of expiration, and it will decay rapidly thereafter until expiration. One can imagine time decay to be like rolling downhill on a bicycle, where the initial speed is much less when the bi-cycle begins rolling down. It gathers speed as it rolls down and hits maximum speed as it reaches the foothill.

Theta and moneyness

The theta value is at its peak when the option is at-the-money. As the options move in-the-money or out-of-the money, very little time value is added, and therefore, theta value is lower. A deep-in-the-money option mostly consists of intrinsic value, and therefore, there is little theta to burn and the rate of theta decay will be less. On the other hand, a deep out-of-the-money option has only extrinsic value, and therefore, it will decay faster during the initial days. However, as expiry approaches, there is little extrinsic value, and therefore, the decay slows down.

Importance of theta

Theta decay is an important factor as it affects the option buyer and seller differently. While theta is a friend to an option seller because as expiration approaches, the option value decreases and one can pocket the difference, for an option buyer theta is an enemy because if the underlying goes against the buyer of the option, theta decay would add to his losses. Moreover, if the underlying stays at-the-money or near-the-money with approaching expiry, the theta decay will quicken. For a directional option trader, the theta decay is offset by the directional movement and the ideal situation will be to make more than what you lose. This means a directional trader should gain more intrinsic value than what he has lost in theta decay. For small underlying moves, It is better to trade options having low theta so that the profits are not eroded from these small moves by the theta lost.

Non-directional trading strategies where you sell a straddle or strangle or any other non-directional strategies use time decay to profit. These strategies would require the right amount of theta value for a profitable trade. However, if the position goes against the original strategy the options available would be to either gain more theta or close the trade. But this comes with its own set of problems.

Things to remember

- Theta is the decline in the time value of an option. The value of an option consists of two parts — intrinsic value and extrinsic value.

- The theta value is at its peak when the option is at-the-money.

- While theta is a friend to an option seller because as expiration approaches the option value decreases and one can pocket the difference, for an option buyer theta is an enemy because if the underlying goes against the buyer of the option, theta decay would add to his losses.

0

|

0

|

0

0