Watch

Watch Spreads are generally a play of two option legs. The name of the strategy depends on how these options are placed.

Traders use two types of spreads – Vertical Spreads and Horizontal Spreads. The name is derived from the two options selected from the options chain table.

If the two options are from the same expiry period but of different strikes, then they are called Vertical Spreads.

If the two options are from different expiries but of the same strike price, then they are called Horizontal Spreads.

There is also a third type of spread that is increasingly gaining traction. It is called a Diagonal Spread. Here the trader selects the two option legs from different strikes and different expiries.

Let’s now take a deep dive into the Horizontal Spread called the Calendar Spread.

Before that, however, there’s a point worth noting. There is a Calendar Spread strategy using futures too. The difference here is that the strategy involves two futures of different expiries, where the trader creates a long futures position in the expiry which is cheaper, and shorts the costlier future of a different expiry of the same underlying.

The rationale for the trade is to create a price-neutral strategy that generates money when the difference between the two futures shrinks.

What Is a Calendar Spread?

A calendar spread is an options strategy created by simultaneously entering a long and a short position on the same underlying but with different expiries.

A long position is created in a far expiry and a short position in the near expiry of the same strike price and same underlying.

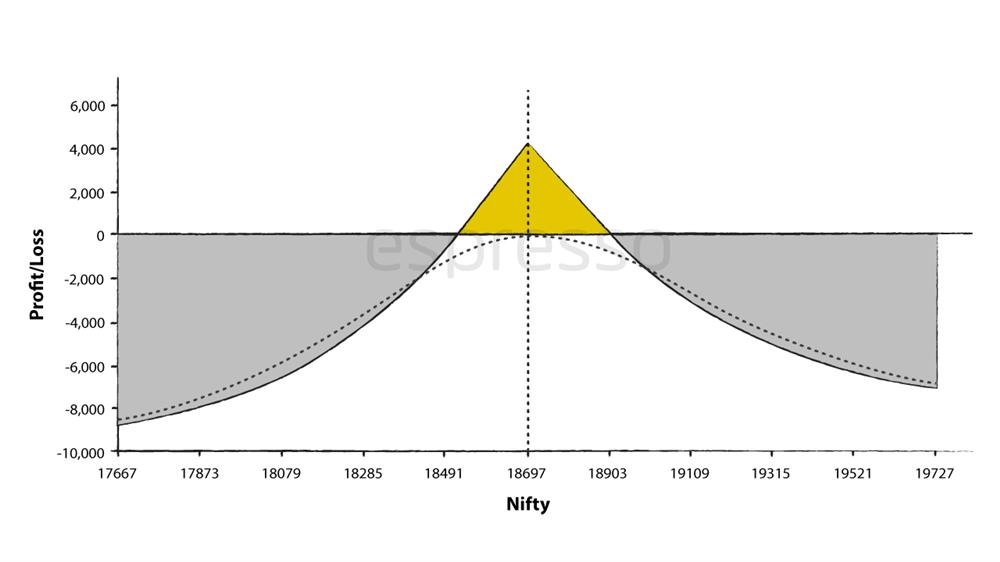

The payoff diagram below shows the calendar spread on Nifty created by using two legs of weekly expiries.

The strategy is created by selling a 18700 Call Option of nearer expiry (December 8, 2022) and buying a 18700 Call of further expiry (December 29, 2022).

The strategy is created by selling a 18700 Call Option of nearer expiry (December 8, 2022) and buying a 18700 Call of further expiry (December 29, 2022).

Note that the calendar spread can be created by either using the Call options or the Put options.

Calendar spread is also called inter-delivery, intra-market, or time spread.

This is a Debit spread strategy, as the value of the premium collected is lesser than the premium paid.

When do we create a Calendar Spread?

The Calendar Spread allows the trader to construct a trade that minimises the effects of time. The strategy is most profitable when the underlying asset remains range-bound and does not make any significant moves.

The calendar spread is created with the intention of profiting from the passage of time and/or an increase in implied volatility (IV).

This strategy is normally created when the trader feels the market is going to remain range-bound, or there will be a slight bullish or bearish movement. The ideal situation is in a low implied volatility environment. Rising volatility after creation of the strategy benefits it.

In case you have a mild directional view that the market is going to be slightly bullish or bearish, you could take the trade by selling a slightly out-of-the-money (OTM) option of the near month, and buying the same strike OTM option of the longer month.

How does a calendar spread benefit a trader?

Here with the passage of time, the near period option will start decaying at a faster rate than the farther expiry option, provided the underlying does not move too much.

However, if implied volatility increases, the farther period option starts making money.

As calendar spreads make money from time and volatility, they are normally created by using at-the-money (ATM) options.

The trade benefits from the behaviour of near- and far-dated options with respect to a change in time and volatility.

All things remaining unchanged, an increase in implied volatility would have a positive impact on the strategy because longer-term options are more sensitive to changes in volatility.

Also, assuming all things remain unchanged, the passage of time would have a positive impact on the strategy till the expiry of the near-term option expiry.

The rate of decay of the near-term option increases with time and will increase as we close on the near options expiry.

A spread strategy requires low capital. In this example, the capital requirement is Rs 26,998, nearly the same as a debit or credit spread created by using options one strike price apart. However, the big differentiator is in return on investment which is nearly 15 percent, compared to 5-7 percent in a vertical spread.

Maximum Loss in a Calendar Spread

Since there are too many moving parts in the strategy, determining the maximum profit and loss is difficult, especially on account of volatility changes that impact the long option.

Nonetheless, there is a theoretical way where we can assume all things remain equal to calculate the maximum loss possible.

Calendar spreads, as mentioned earlier, are debit spreads. The maximum loss in such cases is the amount paid for creating the strategy.

In the example shown above, the amount received for selling a 18700 CE, 08 DECEMBER 2022 option is Rs 105.

The amount paid for buying a 18700 CE 29th December 2022

Thus, the net debit in creating the trade is 295.5-105=190.5

For one lot, the value in rupees works out to Rs 9525

This is the maximum loss in the Calendar Spread strategy.

On the date of expiry, the maximum gain would occur when the price of the underlying asset closes at or below the strike price of the near-term expiry, which would be worthless. If volatility is high on the day of expiry, the far-term option will add to the profitability.

Double Calendar ― When and how to use it, and its benefits

As the name suggests, a Double Calendar Spread is created by using two calendar spreads. It involves selling near expiry calls and puts and buying further expiry calls and puts with the same strike price and same underlying.

Double calendar spread offers a wide range for breakeven and can be deployed in a low-volatility environment.

Let’s now take a close look at the definition of a Double Calendar Spread Strategy.

What Is A Double Calendar Spread?

As was seen in the case of a calendar or time spread, a double calendar spread involves selling an option in one expiration month and buying an option with the same strike price in a different expiration month. A calendar spread is executed with the same type of option ― either a call or a put on both legs of the spread.

A double calendar spread requires the creation of two calendar spreads. A put-based calendar spread is created below the current market, and a call-based calendar spread is created by selecting expiries above the current market.

A double calendar spread is a debit strategy that has positive vega and hence, is created in a 'low-volatility environment'. As volatility picks up, the long options ― calls and puts ― of further expiries start getting profitable.

A long double calendar spread requires purchasing the farther expiry month options and selling the closer expiry options. A short calendar spread requires selling the farther-dated expiry month and buying the nearer expiries.

Short double calendar spreads are rarely traded in practice.

It should be noted that the same number of options contracts are traded on both legs of a double calendar spread (1:1 ratio).

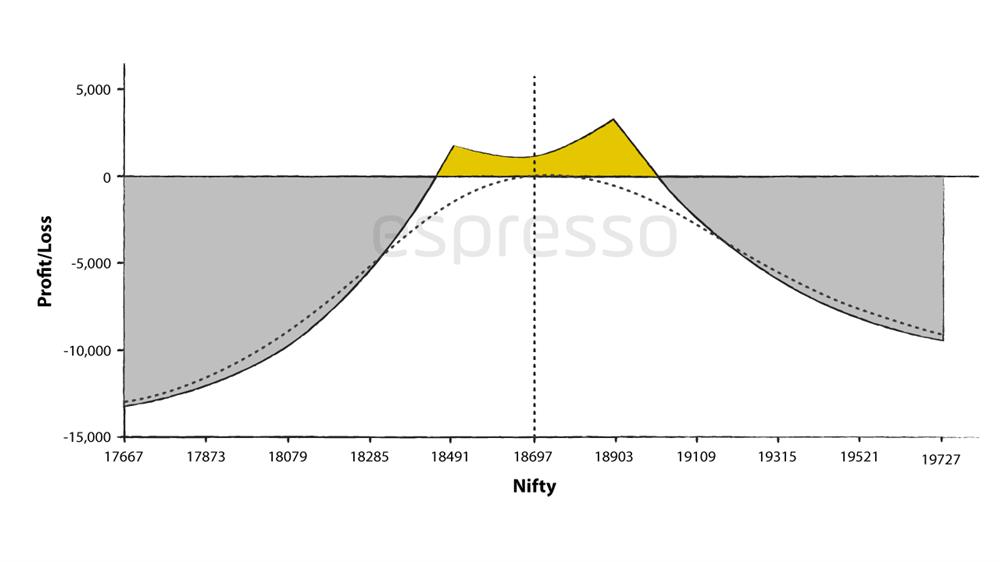

Payoff Diagram

The chart below shows the Payoff Diagrams of a Double Calendar Spread.

Note that double calendars have two profit peaks, which are usually placed above the call and put option strike prices that are sold.

As seen from the pay-off diagram, the double calendar spread was created by selling 18900 08 December 2022 calls and buying 18900 29 December calls on the upper end. The lower end of the double calendar was created by selling the 08 December 18500 Put and buying the 29 December 18500 Put.

As seen from the pay-off diagram, the double calendar spread was created by selling 18900 08 December 2022 calls and buying 18900 29 December calls on the upper end. The lower end of the double calendar was created by selling the 08 December 18500 Put and buying the 29 December 18500 Put.

Notice that the probability of profit from this trade is 71.2 percent. Also, the margin requirement for creating the trade is only Rs 48,261.

The trader makes money if the market remains within the tent till the end of expiry.

Given the fact that the farther expiry options will be open and subject to change to various market forces even as the near expiry options are expiring worthless, it is very difficult to accurately calculate the maximum gain, loss, and breakeven of a double calendar spread. Changing volatility is the biggest contributor to creating this uncertainty.

What is certain is that the trade will make maximum profit when it closes at either of the two peaks, that is, at the strike prices where the calendar spreads have been created.

When to create a Double Calendar Spread

A good time to create a double calendar spread is when the trader expects the market to remain in a narrow range or when volatility is low and is expected to rise.

Take, for example, the credit policy event. If it is expected towards the end of the month, then the trader will buy the call and put options of the month-end expiry and sell the call and put options of earlier expiry. This way, the strategy benefits from higher volatility of the month-end expiry when expectations would be high as to what the RBI governor may announce. At the same time, the earlier options will expire worthless allowing the trader to profit from them.

Note that the theoretical profit of the double calendar spread declines as the underlying moves farther and farther away from the short strike.

Another parameter to look out for while creating a double calendar spread strategy is to look for the condition when the implied volatility (IV) is higher in the nearer expiry options as compared to the farther expiries.

The farther dated option will be costlier on account of the extra time value in its pricing. Since implied volatility plays an important part in the profitability of calendar spreads, it is advisable to sell higher implied volatility and buy lower implied volatility.

Difference between Calendar Spread and Double Calendar Spread

As seen from their construct, while a calendar spread requires buying and selling of either a call or put option of two different expiries, a double calendar spread requires both calls and puts of two expiries for its construction.

Compared to the calendar spread, which is a two-legged strategy, a double calendar spread is a four-legged strategy.

The double calendar spread normally covers a wider space as the trade can be profitable if the price remains between the two tents. With the same premiums, a calendar spread trade will cover a smaller area.

Effectively, a double calendar spread combines a short strangle in the near expiry and a long strangle in the far expiry. On the other hand, a calendar spread is a combination of a short call or put and a long call and a put of different expiries.

Conclusion

A double calendar spread gives a trader extra legroom as compared to a trader taking a calendar spread, albeit on the deployment of a higher margin.

The trade can be taken in a low-volatility environment or when the trader feels that the market will remain range-bound.

A double calendar spread trade is also taken ahead of an event, especially if the event is close to an expiry date. The near-month options will expire worthless if they are out-of-the-money (OTM), while the next expiry option can increase if volatility rises.

0

|

0

|

0

0