Watch

Watch We have learnt about two main types of spreads – vertical and horizontal.

In a vertical spread, we simultaneously buy and sell options of the same type (calls or puts) of the same expiry but different strike prices. The term ‘vertical’ is used because the various strike prices are chosen to select the spread comes from the positions of the strike prices.

A horizontal spread, on the other hand, is an options strategy that involves creating long and short positions in either a call or put option on the same underlying asset and the same strike price but with different expiration months.

A diagonal spread is a combination of the two.

What is a Diagonal Spread?

A diagonal spread involves call or put options of different strike prices and different expiry dates but the same underlying asset.

It is an options strategy created by simultaneously taking a long and short trade in two options of the same type (call or put) but with different strike prices and different expiration dates.

Depending on the structure and the options utilised, the strategy can have a bullish or bearish skew.

A diagonal spread is also called a modified calendar spread because it involves options for different expiry periods. It gets the name ‘diagonal’ because it combines the features of a horizontal spread and a vertical spread.

Construction of a Diagonal Spread

A diagonal spread can be constructed using either a call or put option. The spread needs to be constructed using two options of the same type – either a call or a put.

Different strikes and different expiries are also selected to create a diagonal spread.

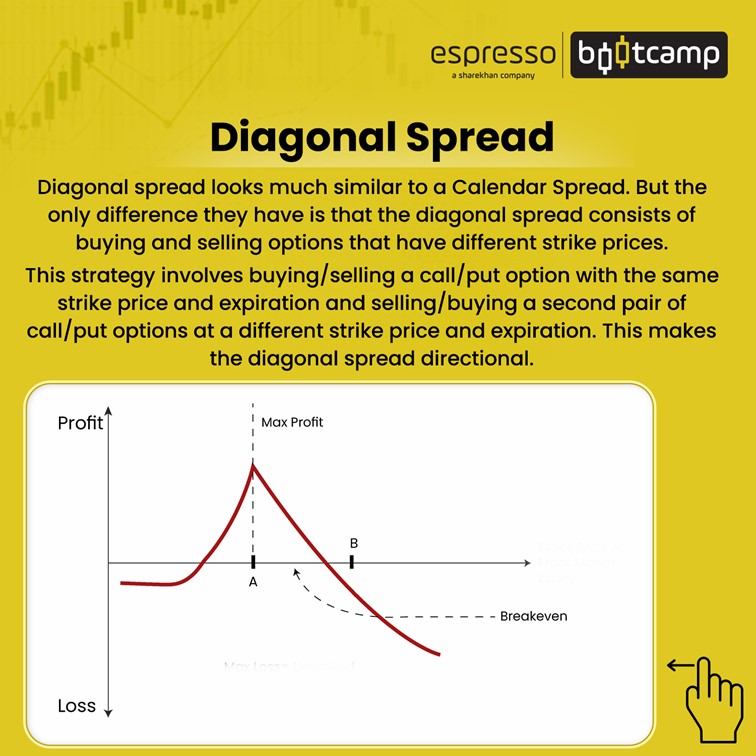

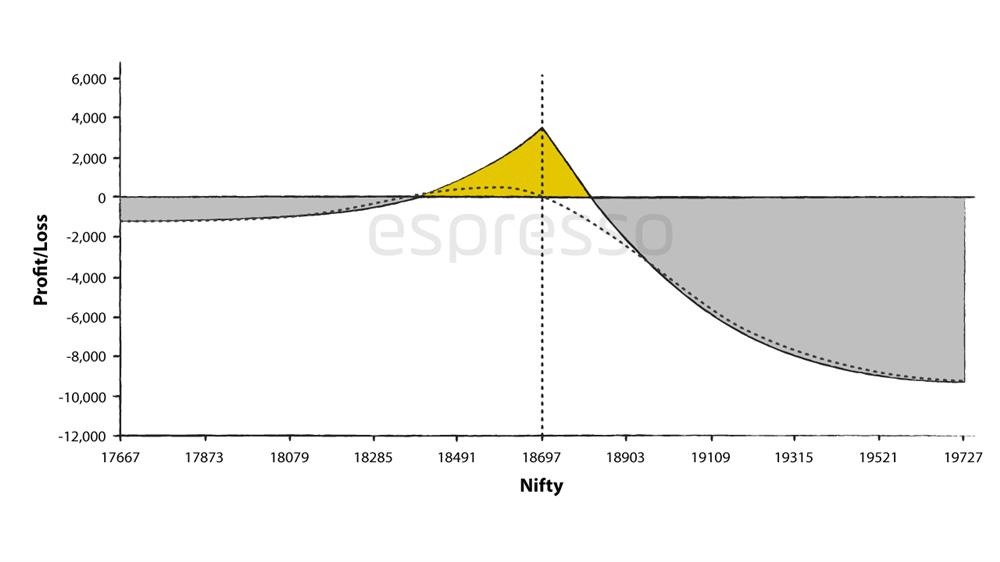

The chart below shows a payoff diagram of a diagonal spread using call options.

The diagonal spread is constructed using 18700 CE and 18900 CE.

A near expiry (December 08) is taken to sell 18,700 CE, and a farther expiry (December 29th) is used to buy a 18900 CE.

Notice the area under the tent – this is where the strategy is profitable.

Though the margin required to create the strategy is small and the return on investment is high, unlike the vertical spread, these numbers change with the market.

The following chart is a payoff diagram of a diagonal spread using put options.

The strategy is created by selling 18700 PE with December 08 expiry and buying 18900 PE with December 29 expiry.

Types of Diagonal Spreads

There are more moving parts in a diagonal spread than in a vertical or a horizontal spread. The number of combinations gives it more flexibility by being bullish or bearish, credit or debit, depending on calls and puts.

Changing the options that are bought and sold and the strikes and expiries, we can arrive at various combinations of diagonal spreads.

The following is a table of some of the permutations and combinations:

| Diagonal Spread Combinations | ||||||

| Option Type | Credit/ Debit | Expiry1 | Expiry2 | Strike 1 | Strike 2 | Direction |

| Calls | Debit | Sell Near | Buy Far | Buy Lower | Sell Higher | Bullish |

| Credit | Buy Lower | Buy Far | Sell Lower | Buy Higher | Bearish | |

| Puts | Debit | Sell Near | Buy Far | Sell Lower | Buy Higher | Bearish |

| Credit | Buy Lower | Sell Far | Buy Lower | Sell Higher | Bullish |

Also, the simplest way to use a diagonal spread is to close the trade when the shorter option expires. However, many traders “roll over” the strategy, usually by replacing the expired option with an option of the same strike price but with the expiration of the longer option (or earlier).

Diagonal spreads are normally constructed like vertical debit spreads, which means the long option is created using the further expiry and the short option by the near expiry.

The strategy is used to take a directional trade with a defined risk while at the same time reducing the cost aggressively by selling a near-term option against the long farther month option.

How does a Diagonal Spread work?

A diagonal spread works like a vertical spread (calendar spread). You will be profitable if the market closes near the short option on expiry.

As the short option is generally near expiry, it will expire worthless if the strike closes out-of-the-money (OTM). Generally, traders close the long option on the expiry of the short option. The long option would still have some extrinsic value left at the time of the expiry of the short option.

However, some traders prefer to roll over their short positions. If the long expiry still has some time left and there are shorter expiries available, traders prefer to hold their long position and create a new short-option position in a near expiry.

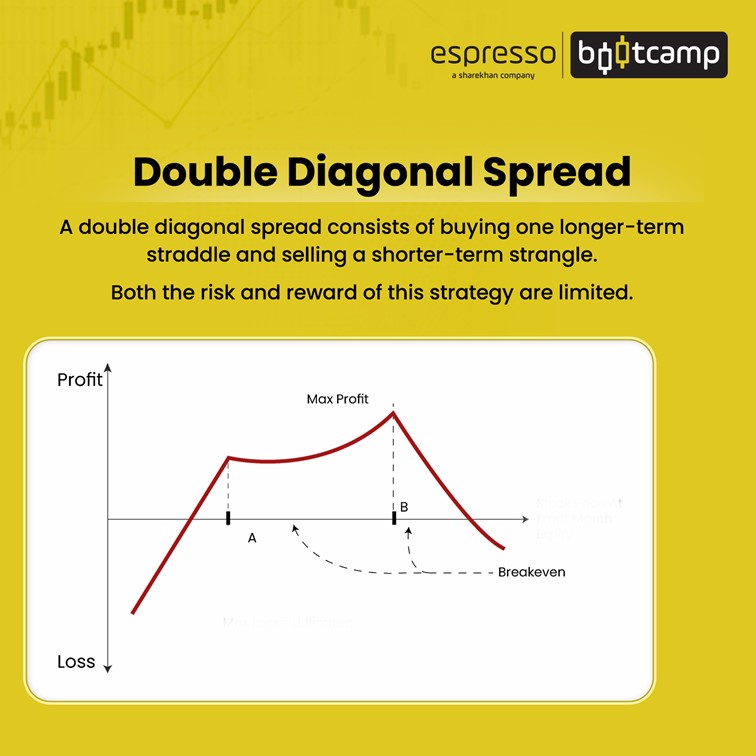

Double Diagonal Spread

A double diagonal spread is an extension of a diagonal spread, just like a double calendar spread.

Double diagonal spreads can be described in either of the two ways. Firstly, they are a combination of a farther-expiry long strangle and a near-expiry short strangle or short straddle.

Secondly, they can be described as a combination of a call diagonal spread and a put diagonal spread.

This is a net debit strategy with both profit and risk being limited.

The maximum profit in the trade is when the underlying asset closes at one of the short options on the near-term expiry.

Construction of a Double Diagonal Spread

A double diagonal spread is created by buying a farther-expiry straddle and selling a near-expiry straddle or a smaller straddle.

Essentially, a trader creates a diagonal call spread and a diagonal put spread. The strategy benefits from theta decay as the sold options of near expiry will decay faster than the bought options of further expiry.

A double diagonal spread is created when the expectation is that the underlying asset will remain between the two sold options till the time of the expiry.

The double diagonal spread may look difficult at first, but if we break it down, it is essentially two diagonal spreads.

Here’s how it is constructed:

· Buy an out-of-the-money (OTM) put of farther expiry

· Sell an out-of-the-money (OTM) put of closer expiry

· Sell an out-of-the-money (OTM) call of farther expiry

· Buy an out-of-the-money (OTM) call of closer expiry

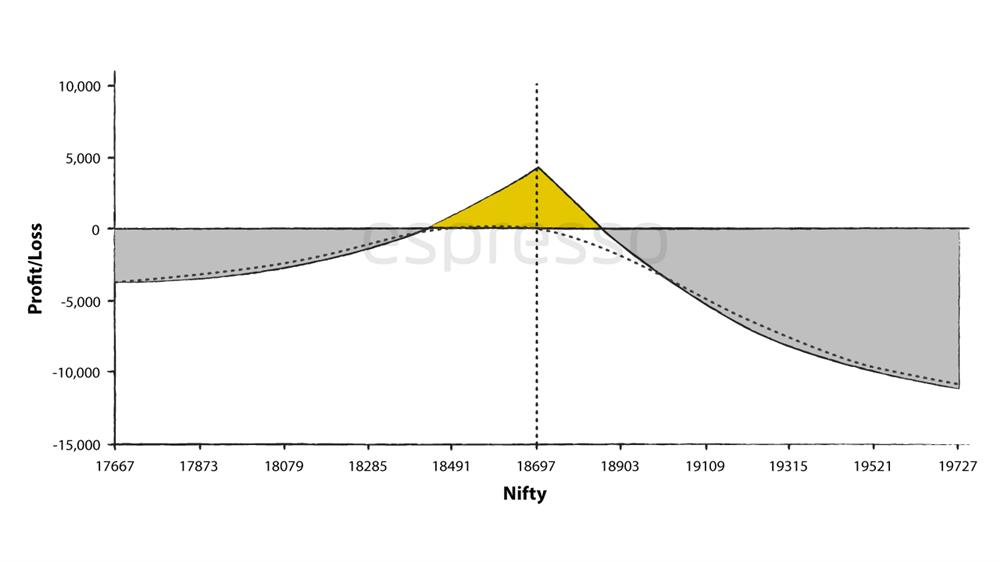

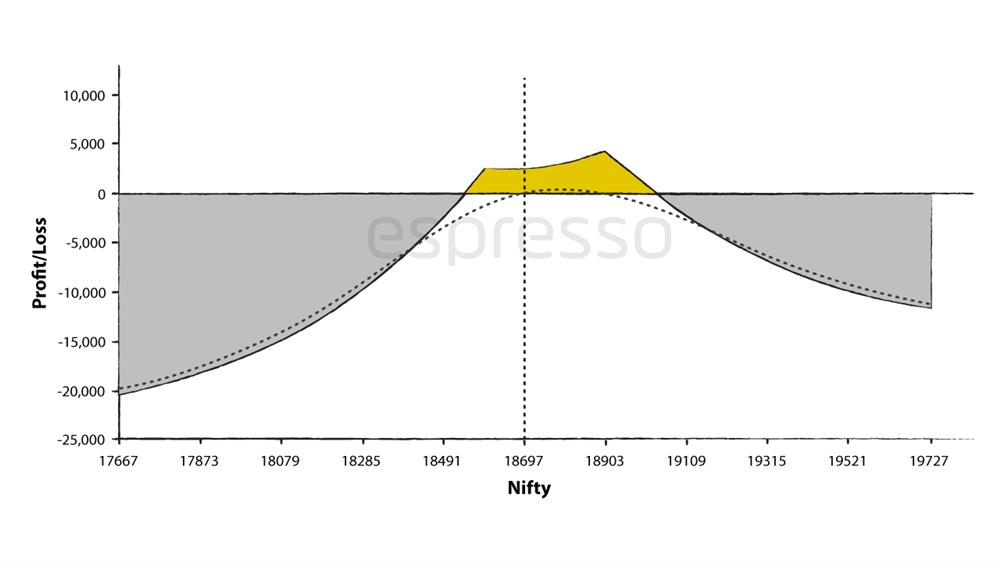

The double diagonal spread is created by selling a near-expiry strangle and buying a longer-expiry strangle of a wider width.

The double diagonal spread is created by selling a near-expiry strangle and buying a longer-expiry strangle of a wider width.

A 18900 call option of December 08 is sold along with a 18600 Put of the same expiry.

Simultaneously 19100 Call and a 18300 Put are bought of December 29 expiry.

The two ‘peaks’ in the payoff diagram are the points at which the near-expiry options are sold.

Breakeven

There are two breakeven points in a double diagonal spread. One is on the call side – between the near-expiry sold call option and the longer-expiry bought call option. The other is on the put side between the sold put option and the bought put option of further expiry.

Determining the exact breakeven point in a diagonal and a double diagonal spread is difficult. While finding the breakeven of a short strangle is easy, combining it with a farther expiry long strangle (creating a double diagonal spread) is difficult because it depends on the level of volatility and price of the long options.

Condition for maximum profitability

Both the diagonal and double diagonal strategies are generally created in a low-volatility scenario.

Even if the price remains stable, these strategies benefit from an increase in volatility. The near-expiry options will benefit from the time decay, while the longer options will benefit from increased volatility.

Double diagonal spreads are highly sensitive to volatility. They will be negatively affected by a fall in volatility, and, alternatively, helped by rising volatility.

Conclusion

Both diagonal spreads and double diagonal spreads are strategies with limited risk and reward potential. They are created when the trader expects small movements in the market. Even if the price remains stable, these strategies benefit from an increase in volatility.

0

|

0

|

0

0