Watch

Watch Vega in options is used to gauge the sensitivity of an option to implied volatility. One needs to be very clear regarding volatility and vega options. Vega is a measure, while volatility is the actual fluctuation that is measured by vega.

Implied volatility is one of the variables used to arrive at options prices. If the price of an underlying is expected to have great movement, the option prices would be expensive, and vice versa. Uncertainty causes higher implied volatility leading to higher price swings and consequently resulting in higher vega.

On the other hand, lack of uncertainty results in lower implied volatility, resulting in lower price swings and, consequently lower vega. Mathematically, vega calculates the variation in option premiums that would occur if implied volatility changed by a percent.

Assume an option with a value of Rs 10. If an option has a vega of 0.10 and the implied volatility drops from 30 percent to 25 percent, the option will lose 0.50 paise, and the option value will drop to Rs 9.50. Similarly, if the implied volatility goes up from 25 percent to 30 percent, the option value would also go up by 0.50 paise, making the value of the options rise to Rs 10.50. Long options have positive vega and short options have negative vega.

Vega, moneyness and expiration

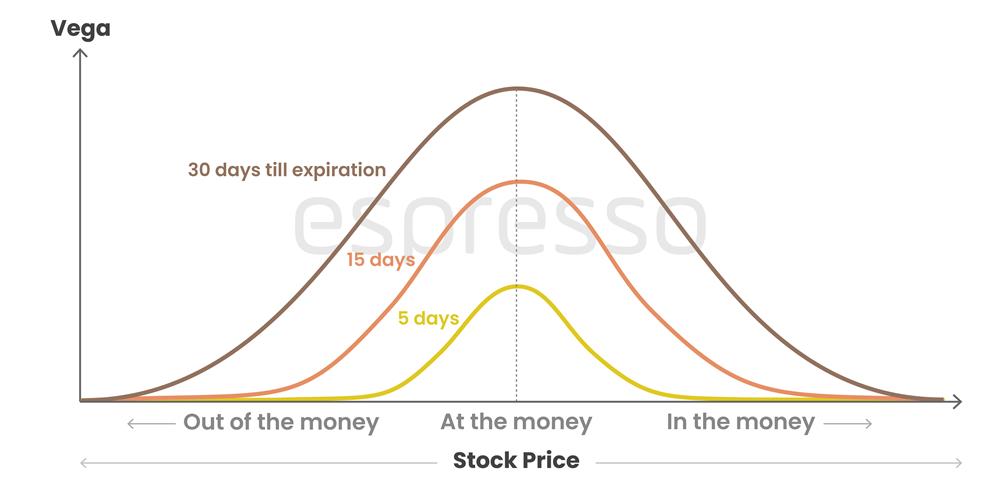

If the expiration of a contract is far away, vega of an option would be high. This is because with more time in hand, uncertainty would be greater and the probability of the underlying running into volatility would be higher. One must understand that time value makes up a large portion of longer period options, and therefore, it is more sensitive to fluctuations. Therefore, the vega is higher for options with longer time expiration. Vega falls as the option expiration nears.

If the expiration of a contract is far away, vega of an option would be high. This is because with more time in hand, uncertainty would be greater and the probability of the underlying running into volatility would be higher. One must understand that time value makes up a large portion of longer period options, and therefore, it is more sensitive to fluctuations. Therefore, the vega is higher for options with longer time expiration. Vega falls as the option expiration nears.

The vega of an option is maximum at-the-money (ATM) and falls as it moves out-of-the-money (OTM) or in-the-money (ITM). The vega for an OTM option is lower as it will need quite a large move of the underlying for the option strike to end in the money. Since vega represents extrinsic value, it does not affect deep in-the-money options as they have very little extrinsic value.

Using vega

Long options have positive vega. A long option holder comes with a directional bias and expects the volatility to increase so that vega increases, resulting in higher premiums and helping him exit at a profit. Short options have a negative vega, and therefore a seller of options would want the volatility to decrease so that the premium decreases and he/she can exit at a profit.

Vega can be used to measure the volatility exposure of a multi-legged option position. If a position is a long vega and the implied volatility is high, then the position could end up making losses as volatility cools off. If, on the other hand, a position is a short vega and the implied volatility is low, one can end up making losses as implied volatility increases.

Therefore, a long vega trade or a position like a long straddle should be initiated when implied volatility is low, and a short vega position like a short straddle should be initiated when implied volatility is high.

Things to remember

- The options Greek, Vega, is used to gauge the sensitivity of an option to implied volatility. Vega is a measure, while volatility is the actual fluctuation that is measured by vega.

- Long options have positive vega, and short options have negative vega.

- Vega is higher for options with longer time expiration. Vega falls as the option expiration nears.

- Vega calculates the variation in option premium if implied volatility changes by a percent.

0

|

0

|

0

0