Watch

Watch We have learnt that spreads are one of the simplest forms of the two-legged options strategy. They are the building blocks of various other strategies.

Spreads have pre-determined risks and rewards and are thus a low-margin instrument that can become a handy tool for a trader.

Spreads, as we learned, are of two types: Credit Spreads, where the trader receives money for creating the spread, and Debit Spreads, where it costs the trader some money to initiate a spread trade.

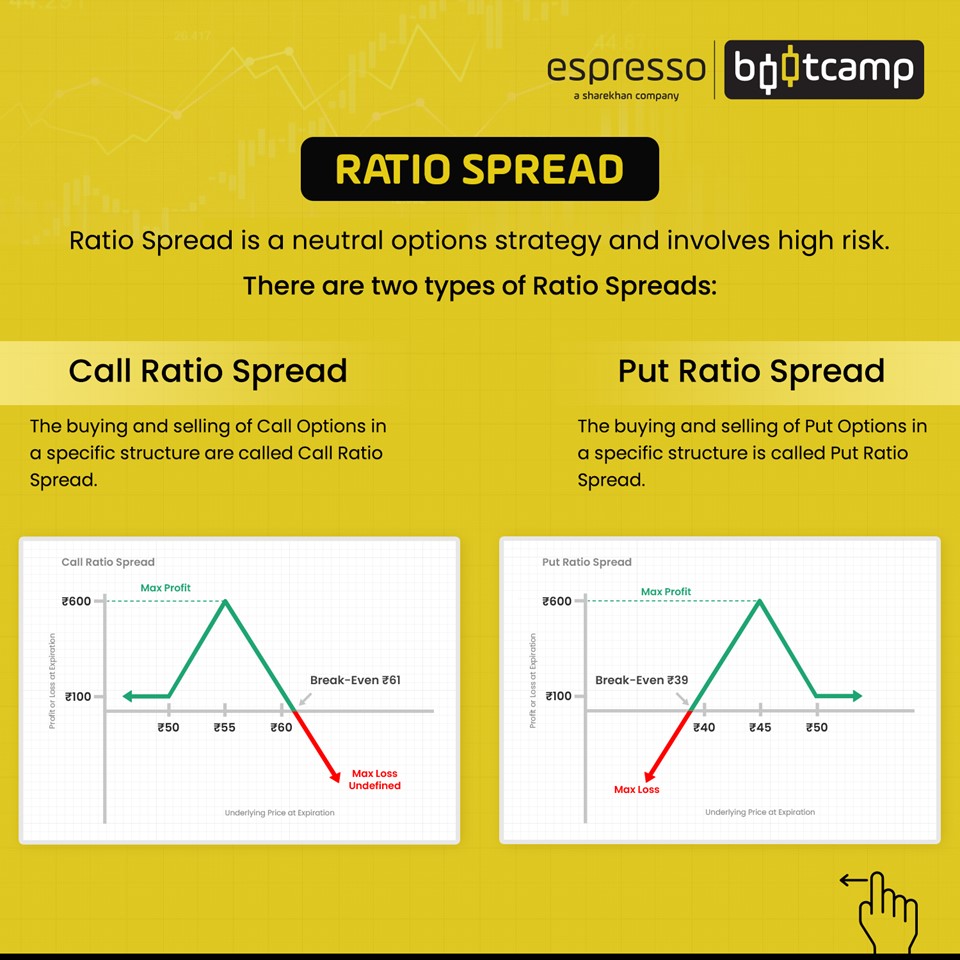

An extension to the spread strategy is called a Ratio Spread. These spreads have a directional bet and a high probability of big profits.

Let’s take a closer look at Ratio Spreads

What is a Ratio Spread?

A Ratio Spread is a trading strategy that is a combination of both long and short options of the same type (call or put). This strategy has an unequal quantity of calls or puts, which allows it to generate high profitability.

While traders have the flexibility of choosing the ratio of options sold to options bought, the most common ratio in a Ratio Spread strategy is 2:1 – which is selling two options and buying one. Or financing the cost of the long spread with the extra short option, making the entire strategy a credit strategy.

Ratio Spreads can be Front Ratio Spreads or Back Ratio Spreads. A Front Ratio Spread has more short contracts than long ones, while a Back Ratio Spread has more long contracts than short ones.

Front Ratio Spreads

A Front Ratio Spread is when a trader creates a call or put debit spread with a higher quantity of short calls or puts at the short strike of the debit spread. This step changes the spread from a net debit to a net credit spread.

The example below shows a Front Ratio Spread using calls.

A debit spread is first created by buying a 18800 call option and selling one 18900 call option. To make it into a Front Ratio Spread, another 18,900 call option is sold.

Notice that the strategy has no risk, in this case, if the market goes down. In most cases, the downside risk will be minimal.

However, the strategy will reach peak profitability if the market closes at the strikes at which the options are sold. The directional bias in this case is moderately upwards.

If the market continues to move higher, profitability will decline and beyond the breakeven point, it will continue to fall and losses will increase.

The chart below shows the Front Ratio Spread using put options.

The payoff diagram is created by buying an at-the-money (ATM) put option and selling an out-of-the-money (OTM) put option to make it a debit spread.

An additional put option is sold to convert the strategy into a Front Ratio Spread, which is a credit strategy.

The strategy has a downward bias and limited loss on the upside. Peak profit in the strategy is at the strikes at which the put options are sold.

Since this is a credit strategy, it works well in a high implied volatility environment.

As for option Greeks, a call Front Ratio Spread has a short delta, which will profit from the underlying moving lower and the strikes expiring around the strikes at which the options are sold.

A put Front Ratio Spread has a long delta, which will profit from the underlying moving higher and the strikes expiring near the strikes at which put options are sold.

Directional Assumption

Front Ratio Spreads are considered Omni-directional trades when we route them for credit because we have no risk and a small profit to the OTM side, but our maximum profit is actually on the in-the-money (ITM) side if our short strike is right on the stock price at expiration.

Put Front Ratio Spreads have a positive delta to start and no risk to the upside, but maximum profit is to the downside at the short strike.

Call Front Ratio Spreads have a negative delta to start and no risk to the downside, but maximum profit is to the upside at the short strike.

Ratio Spread Dynamics

Traders create a ratio strategy when they expect the underlying asset price will remain in a small range. There is generally a small directional bias, depending on the options used (calls or puts) to create the ratio spread.

A slightly bearish trader will create a put ratio spread. A slightly bullish trader will create a call ratio spread.

The ratio is typically between written options and bought options.

The maximum profit for the trade is the difference between the long and short strike prices, plus the net credit received.

There is potential for unlimited loss in the strategy. The one long position (in a 2:1 ratio spread) can only protect the loss of one short position, leaving the trader exposed to the uncovered option.

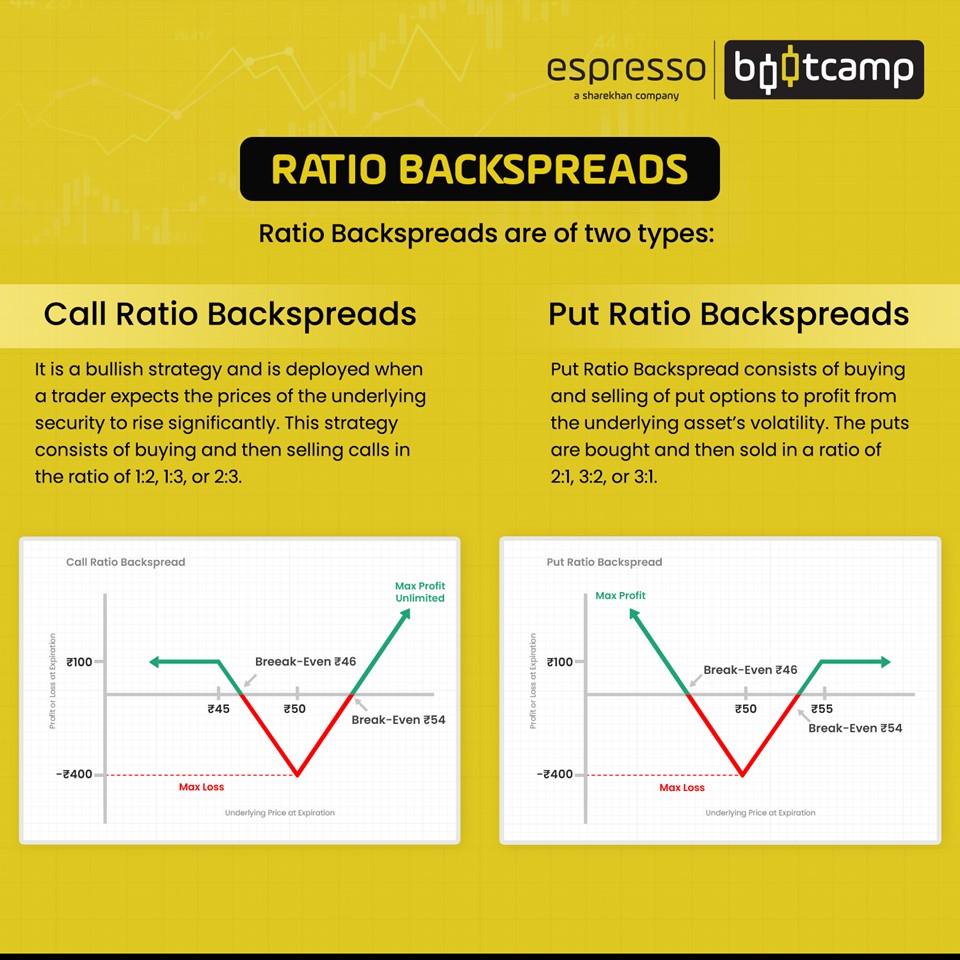

Back Spread

A Ratio Back Spread Strategy is a directional strategy and can be bullish or bearish, depending on the instruments used to construct it.

A call Ratio Back Spread is created when a trader is very bullish on an underlying asset. This is a limited-loss strategy, which will give unlimited profit if the market goes up and a small profit if it goes down.

However, if it stays in a small range, there is potential for a pre-defined loss.

The strategy will lose money only if it remains in a narrow range but will make money if it moves strongly in either direction.

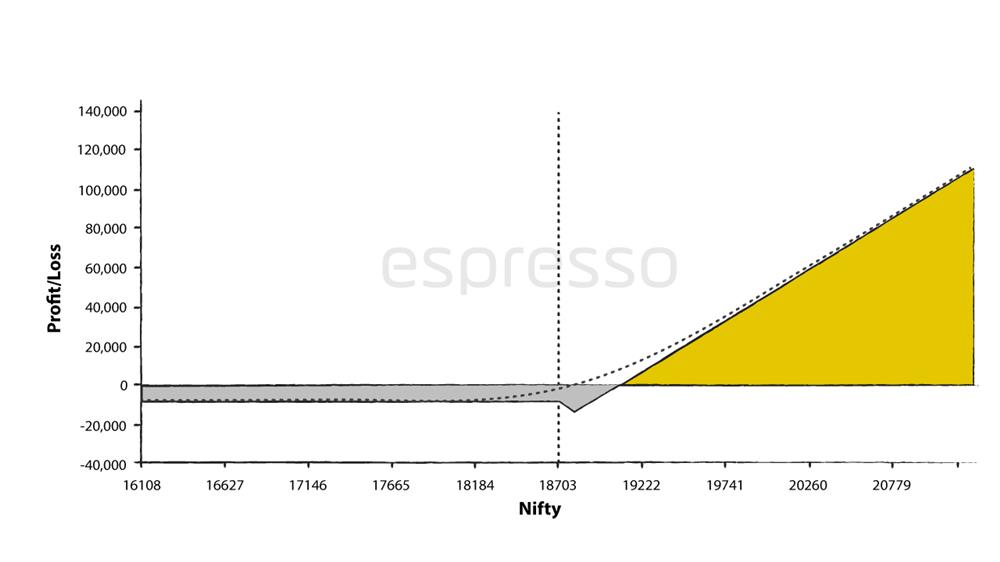

Call Ratio Back Spread

The chart below shows the payoff diagram of a call Ratio Back Spread.

Generally, the call Ratio Back Spread is a credit strategy.

It is the ability to make money in either direction that makes it more popular than buying a call option.

As seen in the payoff diagram, the call Ratio Spread was created by buying two OTM options – 17800 call and selling one ATM or ITM call option – 17700 call.

This strategy has a bullish bias, which can make an unlimited profit if the market moves higher. It will also make a small profit if the market falls.

Losses will occur only when the market remains in a narrow range, with the maximum loss at the strike at which the options were bought.

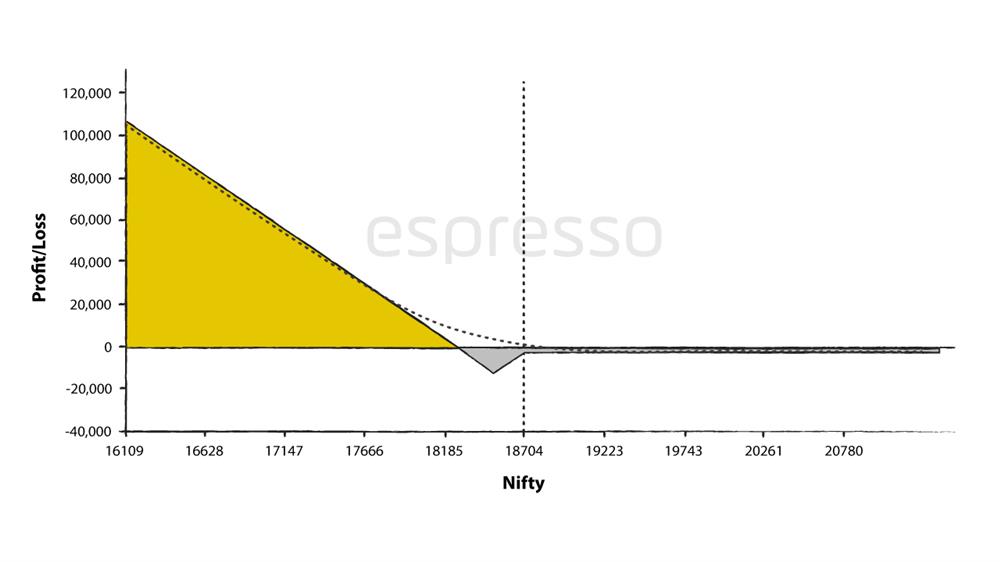

Put Back Spread

The chart shows the payoff diagram of a put Back Spread.

A put Back Spread is created by selling one ATM or ITM put option (18701 put) and buying two OTM options – 18500 put options.

A put Back Spread is created by selling one ATM or ITM put option (18701 put) and buying two OTM options – 18500 put options.A net credit of Rs 0 was generated while creating the strategy.

The Back Spread can generate high profit if the markets continue to fall and a small profit if it rises.

Losses are possible when the market remains in a range, with the maximum loss at the strike at which the options were bought.

Back Spread Dynamics

A Back Spread is a trading strategy that is created by buying more options than selling the same type of options. The most commonly used ratio is 2:1, where two options are bought for every option sold.

A Back Spread can be created by using calls or puts. When call options are used, the strategy is called a Back Spread with a distinct bullish bias. A put Back Spread is deployed when the trader thinks that the market is expected to fall.

A Back Spread is the opposite of a Front Spread where the trader sells more options than he buys.

Conclusion

Spreads are one of the most common options strategies that have a defined profit potential and a pre-determined loss. The strategy is also a building block for other strategies.

Ratio Spreads are the closest cousins of spreads. Here, the basic debit spread is used to construct other strategies like the Front Spread and the Back Spread.

A Front Spread is created when the trader sells more options than he buys. Generally, the ratio is two options sold for each one bought.

A Back Spread is created by buying more options than selling. The commonly used ratio is two options bought for each one sold.

The type of option used to construct the Ratio Spread determines the direction of the spread.

0

|

0

|

0

0