010. Long Strangle and Short Strangle: Types, Greeks and Trade Dynamics

Watch

Watch Another popular trading strategy is called the Strangle. Let's quickly look at what is a strangle in options. Unlike a straddle where the at-the-money (ATM) options are at play, a Strangle strategy is built using out-of-the-money (OTM) strangles.

This is a two-legged non-directional strategy where the trader takes a position in an OTM call, and OTM put options which are at different strikes, but with the same underlying and the same expiration date.

Given the wide choice of strike prices of options to choose from, unlike a straddle, strangle is a popular strategy. Depending on the trader's risk profile, one can choose the strike price to position oneself to trade.

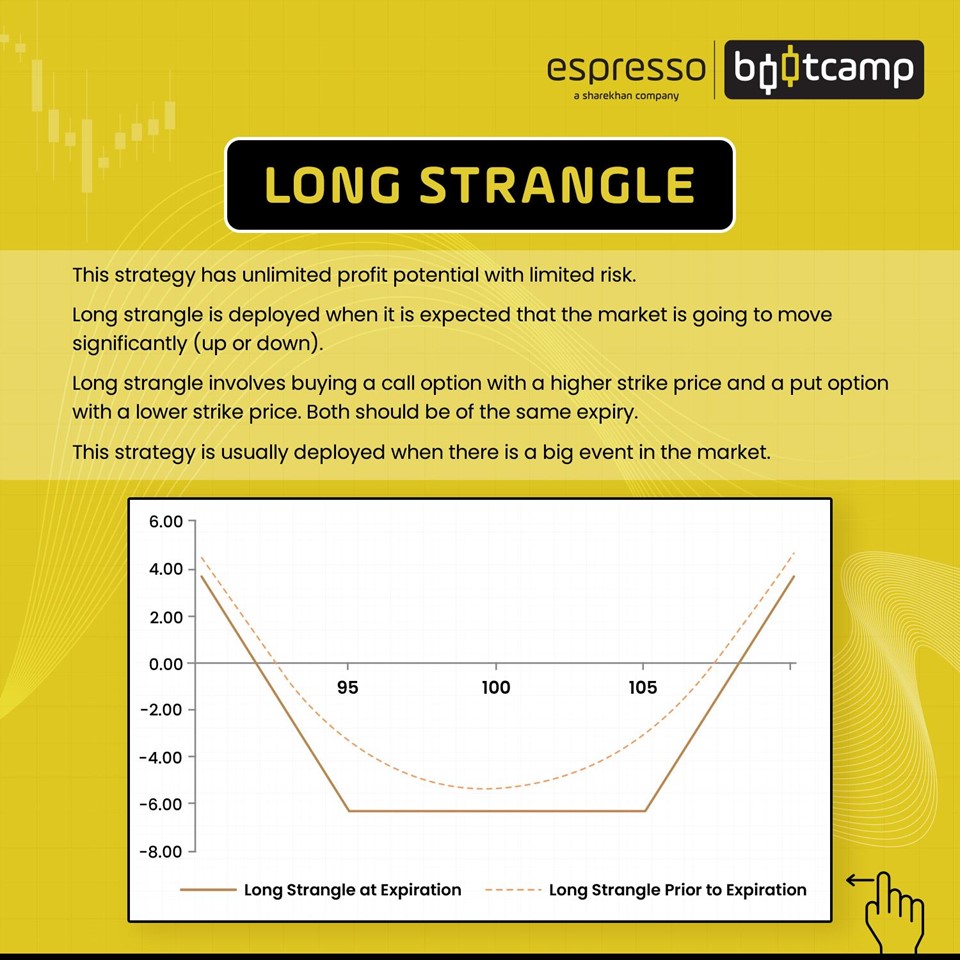

Long Strangle

A long strangle trade is created by buying an OTM call option, and an OTM put option of the same underlying and strike price.

The figure below shows the payoff diagram of a Long Strangle The payoff diagram of a Long Strangle shows Long Call and Long Put positions.

The payoff diagram of a Long Strangle shows Long Call and Long Put positions.

Note that the strike selection of the Call is higher than the current market (CMP), since it is an OTM call option. Similarly, the strike selection of Put is lower than the CMP, as it is an OTM Put option.

Let’s take an example. With Bank Nifty trading at 43103, a Call option of 43200 strike and a Put option of 43000 is selected.

A call option is bought for Rs 226, and a put option is bought for Rs 189.2.

Expiry dates for both options are 08 DEC 2022.

Since the lot size is 25, the cost of buying the call option is Rs 5650 (Rs 226 X 25 = Rs 5650), and the cost of buying a Put option is Rs 4,730 (Rs 189.2 X 25 = Rs 4,730).

The cost of holding the trade is the total of the two, which is Rs 10,380.

This is also the maximum a trader can expect to lose from the trade.

Since the trader has bought the options, he holds a position offering unlimited profit potential.

However, the problem with OTM options is that they need a strong move in the underlying in order to give positive returns. In this case, the probability of profit is only 46.75 percent, though the potential is unlimited profit.

Trade Dynamics

The cost of buying the strangle is Rs 5,650 + Rs 4730 = Rs 10,380 for one lot of Bank Nifty. This is also the maximum loss that the trader will incur in this trade if he holds the position till expiry.

The trade will post a maximum loss between the two strike prices on which the options have been bought.

Thus, the strangle will be in a losing position if on the day of expiry, Bank Nifty closes between 43000 and 43200.

The trade will break even if the Bank Nifty moves above the strike price of the options bought plus the cost incurred in buying them.

The cost of buying the option is:

Cost of buying the Call option + cost of buying a Put option = 226+189.2=415.2

Thus, the breakeven on the call side is 43200+415=43615.2

And the breakeven on the lower side is 43000-415.2=42,584 =

The profit potential is virtually unlimited, so long as the price moves beyond the breakeven.

This is a risk-defined strategy where the trader knows upfront the maximum loss that he could incur by taking the position.

Greeks in Long Strangle

A long straddle strategy is considered to be a non-directional strategy. Though many traders try to make the strategy a Delta-neutral one by buying options having the same delta, there is always some skew, especially when the trader tries to maintain the same strike distance from the current market.

In the above example, the delta of the 43200 long calls was +45.81, while that of 43000 long puts was -41.65, making the net delta of the strategy at 4.16.

Like the long straddle, long strangle trades are also taken closer to an event when the trader expects a sharp move in either direction.

As in the case of the long straddles, theta has a role to play here. If the days to expiration are close, theta will impact the strategy's profitability. But if the expiration day is far away, theta will have minimal impact.

The flexibility that strangles offer over straddle is the choice of Strikes. Depending on the traders' risk profile and the gravity of the event, traders pick up their strikes to create a long strangle trade.

They can select a low premium or a low delta strike if the expectation is of a very big move. But if they expect a sharp and fast move, but not so significant, like in an earnings trade, they would create a Long Strangle by choosing strikes closer to the market.

Volatility also is an important Greek to consider before deploying the strategy. Long strangles are taken when volatility is low, which keeps premium prices low and, thus, the cost of buying low. A low-volatility environment offers a good risk-reward trade.

A low volatility scenario also suggests that the market is not expecting much from the event. In other words, it is more likely to be a non-event and the underlying will not move much.

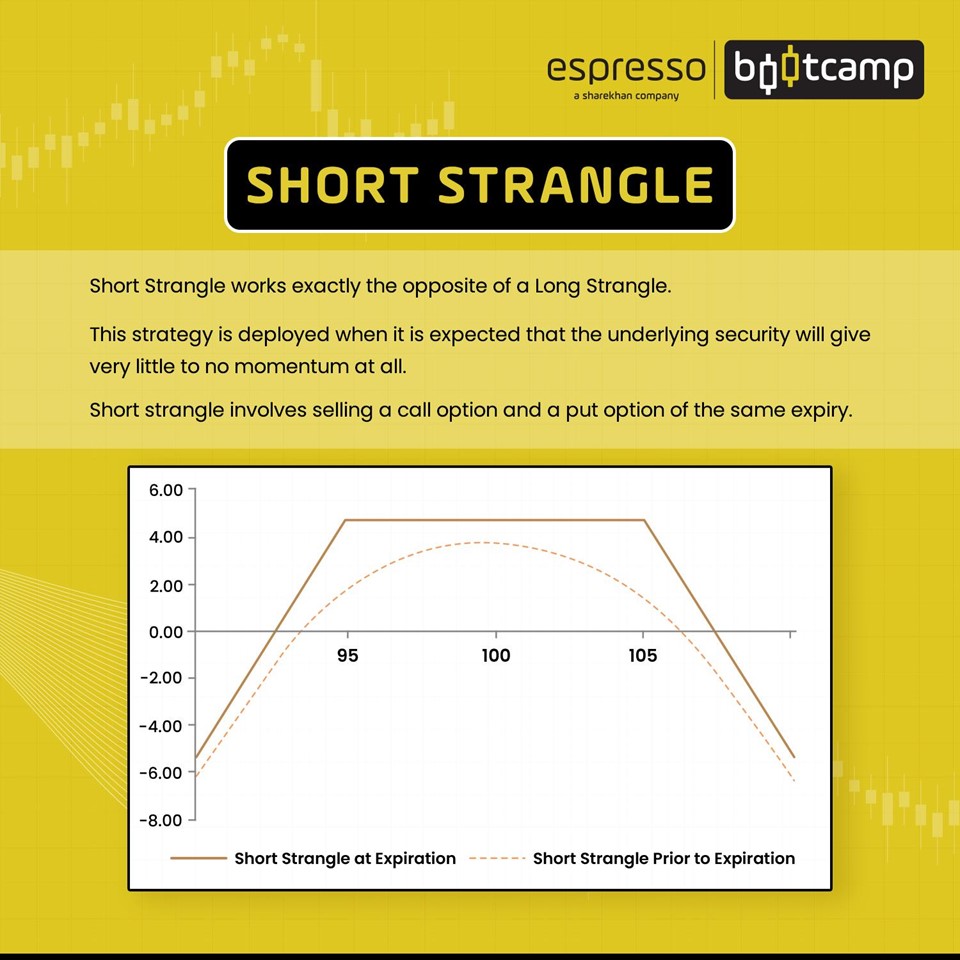

Short Strangle

As in the case of Short Straddle, a short strangle is also a popular strategy among intraday traders. The concept remains the same, taking advantage of time decay.

A Short Strangle is created by selling OTM call and put options.

The chart below shows the payoff diagram of a short strangle trade.

The trade is created when the trader expects the underlying to close between the two strikes he has sold at the expiry time.

In the above example, the trader expects Bank Nifty to stay between 43000 and 43200 till 08th DEC, the expiry date.

The same strikes in the case of the Long Strangle have been selected, that is, a Short 43200 Call and a Short 43000 Put option.

While shorting the two options, the trader collected 415.2 points per unit of Bank Nifty.

Considering the lot size of 25, the premium collected in creating the strategy is Rs 10,380.

The margin required for creating the Short Strangle trade is around Rs 1,65,974.

If Bank Nifty closes between 43000 and 43200the trader will pocket the entire premium of Rs 10,380, thus yielding a return of around 6.25% percent.

Expiry dates for both options are December 08 2022.

The drawback of this strategy is that it has a potential of unlimited loss if Bank Nifty moves beyond 43000 or 43200.

Unlike the Long Strangle trade, the probability of profit in a Short Strangle trade is 53.24% percent.

Trade Dynamics

The 43200 CE is sold at Rs 226

The 43000 PE is sold at Rs 189.2

The net points collected per unit of BankNifty is Rs.415.2

The net premium collected per lot of Bank Nifty (25 units) is Rs 10,380

Maximum profit in trade = Net Premium collected = Rs 10,380

Note this peak profit is possible if the market closes between 43000 and 43200

The margin required for creating this strategy is Rs 1,65,974

Maximum loss is unlimited

The trade will be profitable only if Bank Nifty stays within the shaded area

Thus, the breakeven on the long side is 43200+415.2 = 43615.2

And the breakeven on the lower side is 43000-415.2 = 42,584.8

The short strangle is a non-directional strategy where the potential for loss is unlimited and the strategy offers a limited but high probability profit potential.

Greeks in Short Straddle

Strangle strategy is built using out-of-the-money (OTM) strangles. This is a two-legged non-directional strategy where the trader takes a position in an OTM call, and OTM put options that are at different strikes, but with the same underlying and the same expiration date.

A short strangle strategy is a non-directional strategy that can be made a Delta-neutral strategy at the initiation.

If the deltas of the call and put sides are matched, then the net delta of the strategy will be zero at the time of initiation.

Theta is the main Greek that a short strangle trader tries to capitalise on. The trade makes money if the market moves in a narrow range and there is continuous theta decay.

Short strangle trades are mostly taken on the current expiry options as they will be decaying faster than later-dated expiries.

Many professional traders use short strangle strategies on event days as volatility is high, and the trader gets a wide range to play with (selection of option strikes) as well as collects a high premium. Return on investment is high in such a scenario.

Volatility plays an important part in this strategy. The higher the volatility as measured by the Implied Volatility Rank (IVR) or Implied Volatility Percentile (IVP) better is the Return on Investment in the trade and the wider the breakeven point.

Conclusion

After straddles, strangles are probably the most common strategy. In fact, retail traders prefer strangles over straddles as they can play with smaller premiums by selecting deep OTM option strikes. Professional traders prefer the short straddle over the long straddle as the probability of success is better in selling options.

Things to remember

ATM options are at play in a straddle, while a Strangle strategy is built using OTM strangles. This is a two-legged non-directional strategy where the trader takes a position in an OTM call, and OTM put options at different strikes but with the same underlying and expiration date.

Straddles and strangles are both commonly used strategies.

Retail traders prefer strangles over straddles, as they can play with smaller premiums by selecting deep OTM option strikes.

Professional traders prefer the short straddle, as the probability of success is better in selling options.

0

|

0

|

0

0