014. Butterfly Strategy: All about Call, Put and Iron Fly Butterflies

Watch

Watch Some of the most popular and commonly used strategies in options are non-directional or neutral strategies. These strategies try to capitalise on the fact that the market is non-trending or sideways 70 percent of the time and trending upward or downward only 30 percent of the time.

We will now look at another popular non-directional strategy called the Butterfly Strategy.

The name is said to have originated from the payoff diagram, with the peak looking like the body of a butterfly and horizontal lines that appear like its wings.

What is the Butterfly Strategy?

The Butterfly Strategy is a non-directional strategy that is created by combining a bull and a bear spread. Since spreads have pre-defined risk and reward levels, the same applies to the Butterfly Strategy. The risk is fixed and the profits are capped in the Butterfly Strategy.

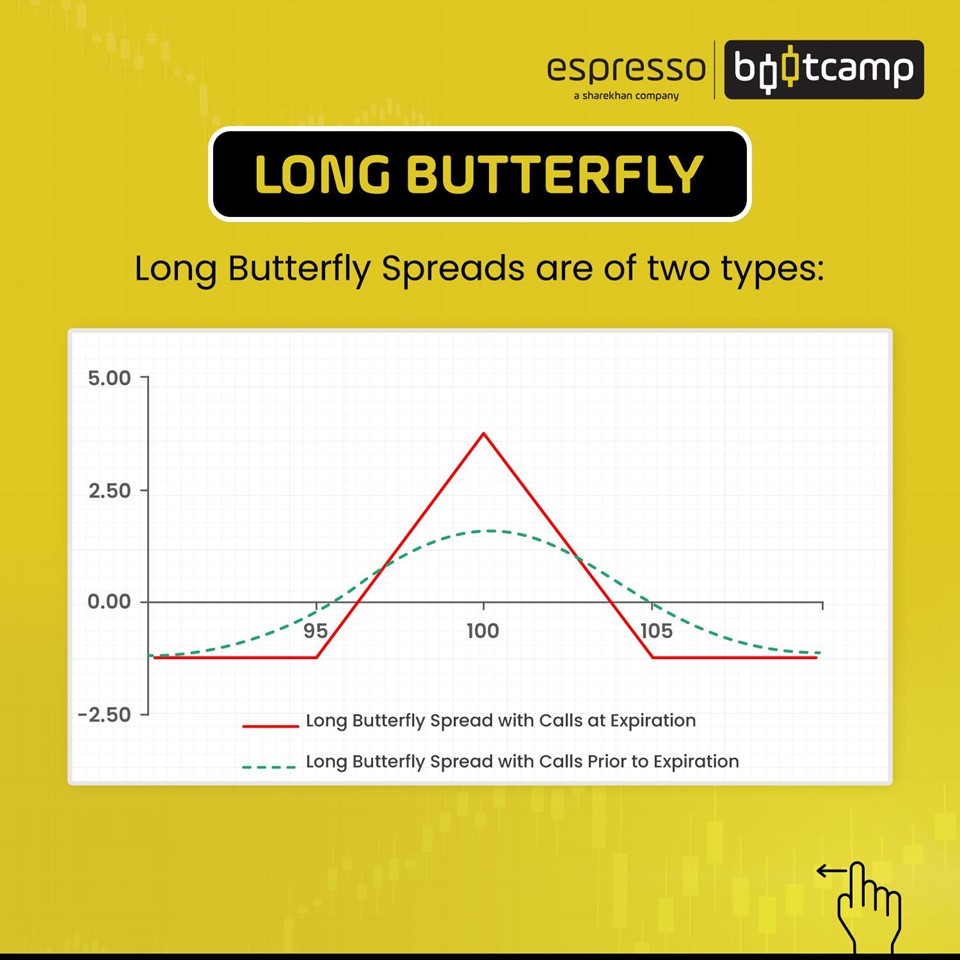

The strategy achieves maximum profit if the market remains in a small range till the options expire.

These spreads use four options and three different strike prices. The strategy involves four calls or four puts, or a modification called Iron Fly, which is a combination of puts and calls with three strike prices.

The upper and lower strikes of the strategy are at equal distances from the middle. The strikes for the options in the centre are selected depending on the trader's view.

Understanding Butterfly Spreads

Non-directional traders normally use the four-legged Butterfly Strategy.

This is done by adding a bull spread to a bear spread.

Three strikes are involved in creating the strategy:

-An out-of-the-money (OTM) strike price call or put

-An at-the-money (ATM) strike call or put

-An in-the-money (ITM) strike call or put

While creating a Butterfly Strategy, the trader must use all call or put options. Also, the OTM strikes and ITM strikes should be at the same distance from the ATM strike options.

If calls are used to create the strategy, and if the ATM strike is at 18650 and the ITM strike is at 18,450, then the OTM strike should be at 18,850. The distance between the two strikes should be the same, which, in this case, is 200.

Both calls and puts can be used to create Butterflies.

Constructing the Butterfly Strategy

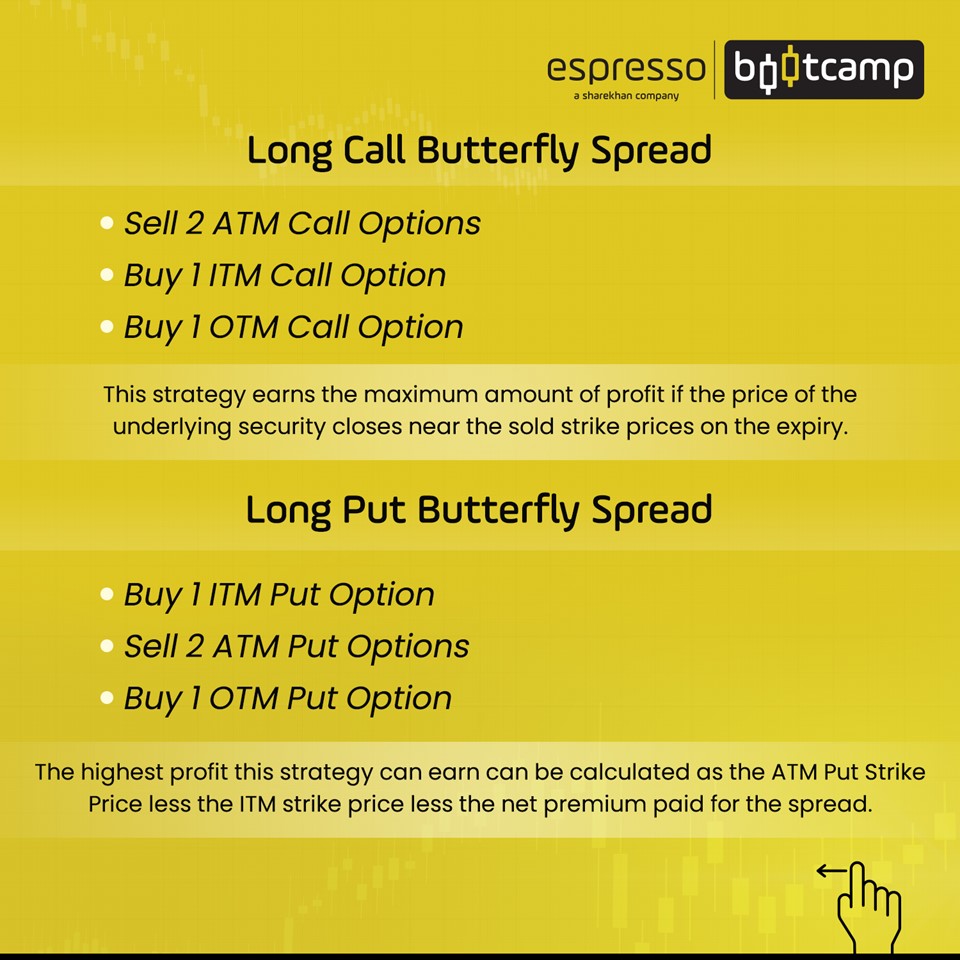

Here is how a Butterfly Strategy is constructed using call options.

Call Butterfly

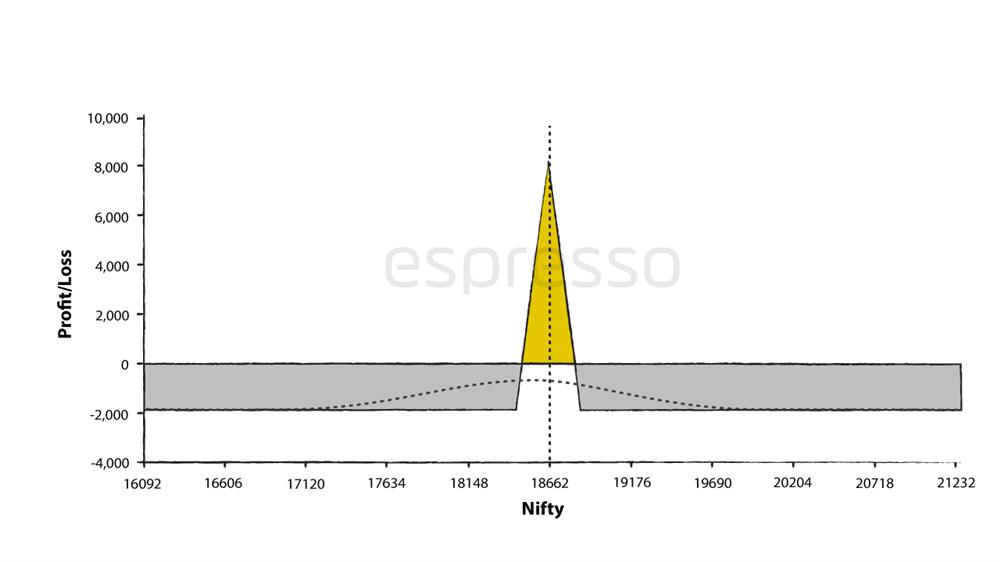

The payoff diagram below is of a Butterfly Strategy using Nifty call options.

The call Butterfly Strategy is created with the Nifty at 18,667.8.

Two ATM call options (18,650) are sold at Rs 300.7

One ITM Call Option (18,450) is bought at Rs 437.45

One OTM Call Option (18,850) is bought at Rs 201

The Butterfly Strategy has a maximum profit potential of Rs 8,148 if the market closes at 16,650, which falls sharply after that point. The maximum loss is Rs 1,852.

The breakeven points are 18,488 and 18,812, giving a range of 318 for the strategy to play in.

The margin required for creating a Butterfly Strategy is Rs 37,903.

The strategy offers a good risk-to-reward ratio of almost 1:4.

The maximum loss is the net cost paid to create the strategy, which, in this case, is Rs 1,852, or 37.04 ((300.7 X 2)-437.45-201).

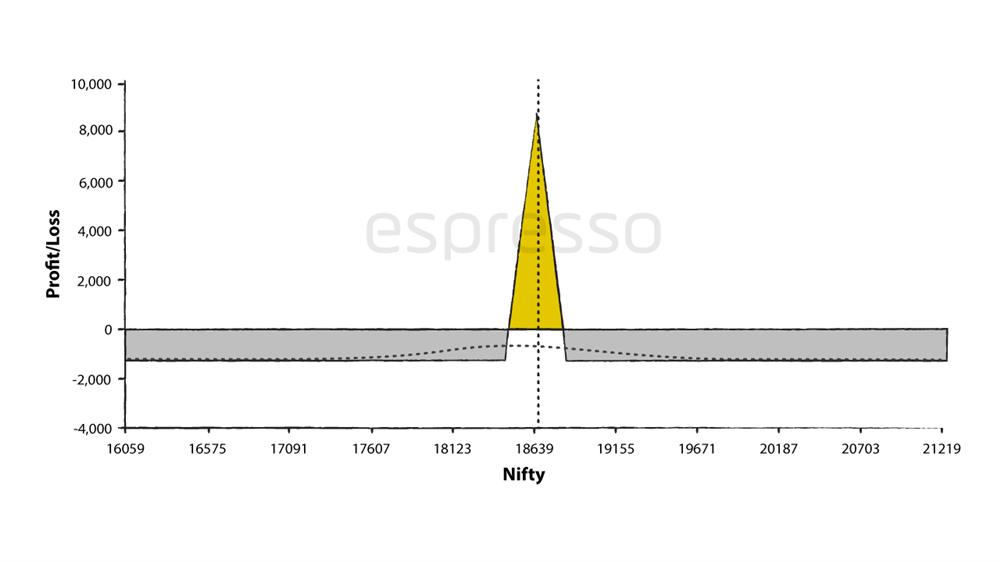

Put Butterfly

The payoff diagram below is of a put Butterfly.

Two ATM put options (18,650) are sold at Rs 178.2

One ITM Put Option (18,850) is bought at Rs 266.15

One OTM Put Option (18,450) is bought at Rs 116

The Butterfly has a maximum profit potential of Rs 8,713 if the market closes at 18,650, which falls sharply after that point. The maximum loss is Rs 1288.

The breakeven points are 18476 and 18,824, giving a range of 322 for the strategy to play in.

The margin required for creating a Butterfly strategy is Rs 37,853.

The strategy offers a good risk-to-reward ratio of almost 1:4.

The maximum loss is the net cost paid to create the strategy, which, in this case, is Rs 1,288, or 25.76 ((178.2 X 2)-266.15-116).

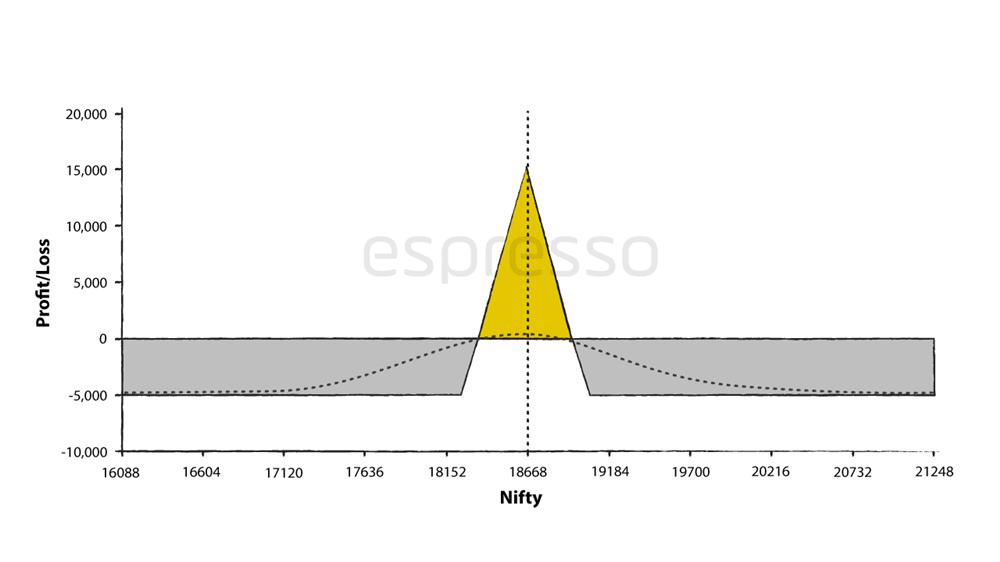

Iron Fly

A modification of the Butterfly Strategy is the Iron Fly. The difference is that the sold options are calls and puts. In other words, a short Straddle with insurance on both sides is called an Iron Fly.

The payoff diagram below is of an Iron Fly.

As can be seen from the payoff diagram, it is created by:

Selling an ATM call option 18,650 at Rs 310

Selling an ATM put option 18,650 at Rs 172.1

Buying an OTM call option 19050 at Rs 109.2

Buying an OTM put option 18,250 at Rs 71.4

The Iron Fly has a maximum profit potential of Rs 15,075 if the market closes at 18,650, which falls sharply after that point. The maximum loss in the strategy is Rs 4,925.

The breakeven points are 18,349 and 18,951, giving a range of 602 for the strategy to play in.

The margin required for creating the Iron Fly Strategy is Rs 62,693.

The strategy offers a lower risk-to-reward ratio than the Butterfly Strategy at 1:3:06.

When to create a Butterfly Strategy

By default, a Butterfly Strategy is created when the trader expects the market to remain flat or unchanged.

A long Butterfly Strategy constructed using call options realises its highest profit if the stock price equals the centre strike price on the expiration date.

A call Butterfly is created when the trader thinks the market is expected to be rangebound to slightly bearish.

If the trader feels the market will be moderately bearish, he will create the strategy when the sold options at the centre are a strike or two below where the market is.

In the case of a moderately bullish outlook, a put Butterfly can be created with the sold options being a strike or two above the current market price.

Strategy Dynamics

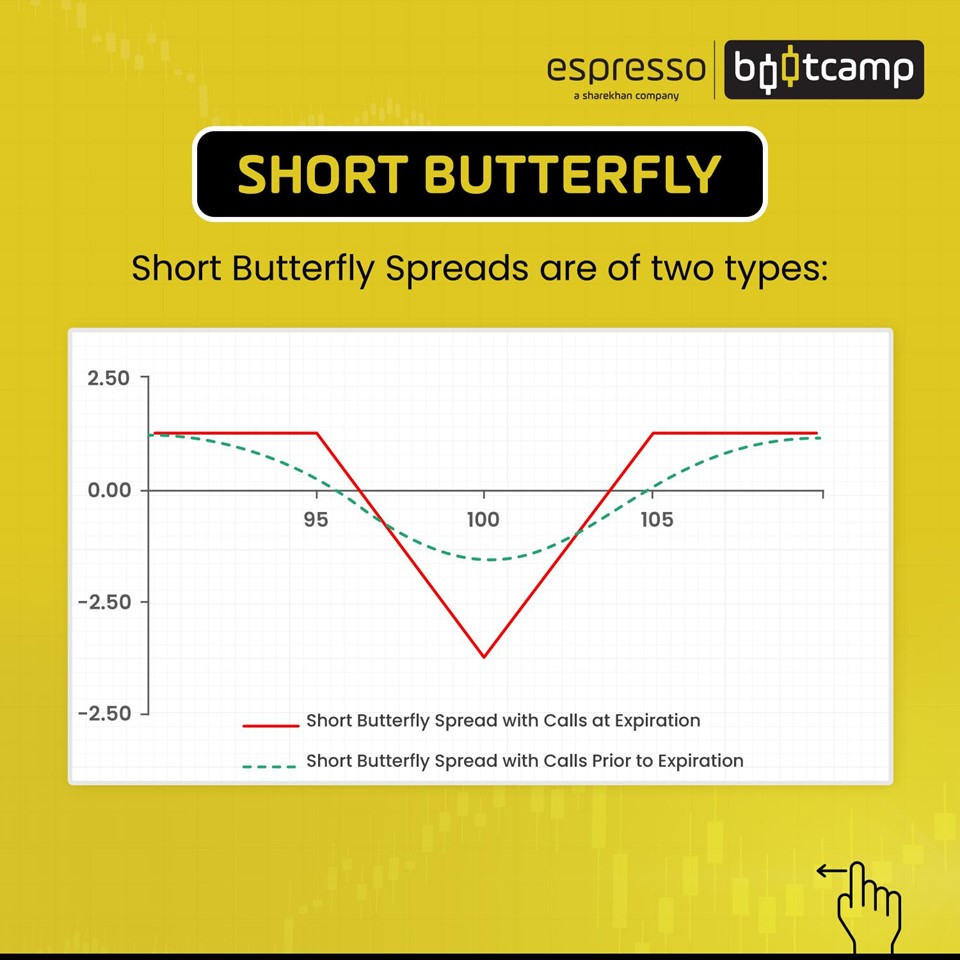

What makes Butterflies different from other non-directional strategies such as Straddle and Strangle is that it is a four-legged strategy with its risk defined.

However, the controlled risk comes at the cost of the two options that are bought. This reduces the potential profit from the trade. A Butterfly trade has much lower profit potential.

The Butterfly Strategy is sensitive to volatility changes. The net credit of a Butterfly spread falls when volatility rises and increases when volatility declines.

Proficient traders buy Butterfly Strategies when they expect volatility to fall.

Butterflies are good strategies to trade when volatility is expected to fall sharply after an event such as earnings or the budget.

The big attraction for the strategy is the high risk-to-reward ratio, the low margin required to create one, and the high return on investment (ROI).

Impact of Greeks on the Butterfly Strategy

Delta

Delta is the options Greek that measures how much an option price varies with changes in the underlying price. Since a Butterfly Strategy has three options, too many moving parts affect its performance.

Long call options will have a positive delta, while short ones will have negative deltas. Long puts will have a negative delta, while short puts will have a positive delta.

If, in a call, Butterfly, the underlying price is below the lowest strike price, then the net delta is slightly positive, while if the underlying price is above the highest strike price, it is slightly negative.

Vega

Option prices rise with an increase in volatility and fall as volatility shrinks. Vega measures the effect of a change in volatility on option prices.

Long options, either call or put, will rise with an increase in volatility, while short options trades will incur losses when volatility rises. Similarly, long options will lose value when volatility falls, while short option trades will be profitable.

A Butterfly Strategy with calls has a negative Vega, which means the strategy will lose money when volatility rises. When volatility falls, a long butterfly strategy will make money.

The thumb rule of trading Butterfly Strategy is to buy one when volatility is high and expected to drop.

Theta

Theta measures the impact of time on option prices.

Options are decaying instruments that lose value with time. Long options have a negative theta and will lose value over time, with other factors remaining constant. Short options will generate profit with time as they have a positive theta.

Conclusion

A Butterfly Strategy is created by combining a bull call spread and a bear call spread. The strategy is created when a trader expects the market movement to be flat, slightly bullish, and bearish.

A Butterfly Strategy can be created using call options or put options.

Iron Fly, a modified Butterfly, is created by using two pairs of call and put options.

0

|

0

|

0

0