Watch

Watch Buying a Put Option is the usual strategy a trader adopts in a weak or falling market. Put options are preferred by the trader over Futures because his potential maximum losses are predefined, which makes his risk-reward profile much simpler. A trader usually charts his risk rewards in trade through call/put payoff diagrams.

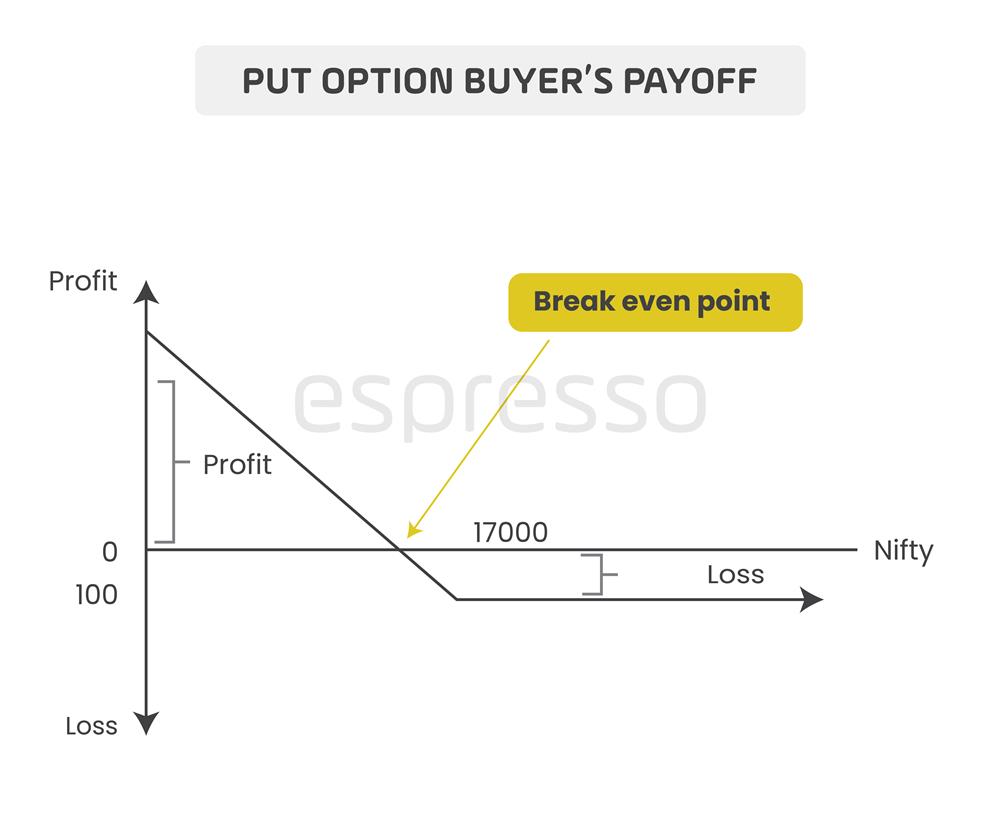

A put payoff diagram explains the profit/loss from the put option on expiration and the breakeven point of the transaction. It’s a pictorial representation of the possible results of your action (of buying a Put).

If you have bought a Put option, you will be hoping to see the price of the underlying to go down because the lower it goes vis-à-vis the strike price, the greater will be your profit. In other words, by taking a long put option position, you will make money when the price of the underlying goes down, and you will lose if it goes up.

In the above diagram, profits/losses of a trader who has bought three months Nifty Put option at 17,000 are clearly shown. Let’s assume that the buyer buys Put option for a premium of Rs 100. In other words, he spends Rs 5,000 (Rs 100 X one lot of Nifty, i.e., 50). This means that his breakeven point becomes 16,900, i.e., 17,000 – a premium of Rs 100. Thus, the trader will start making a profit only when the spot price falls below 16,900 or when the strike price becomes in the money (ITM). His profit will go on increasing as Nifty continues to touch lower levels. On expiration, if Nifty closes below the strike of 17,000-100, the buyer of the Put would naturally exercise his option and, in the process, make a profit to the extent of the difference between 16,900 and Nifty-close. Anywhere above the breakeven point, the option would not be favourable to the trader and he will not able to exercise his option. On the other hand, if Nifty closes below the breakeven point on expiry day, the trader will make a profit, and the amount of profit will depend on the spot price closing on expiration. From the above diagram, it is also clear that, theoretically, the profits possible for the buyer on this option are unlimited.

Based on the above example, the trader’s P&L table will appear as follows:

| On expiry Nifty closes at | PE buyer’s payoff |

| 16700 | 200 |

| 16800 | 100 |

| 16900 | 0 |

| 17000 | -100 |

| 17100 | -100 |

| 17200 | -100 |

| 17300 | -100 |

From the above table, it is clear that though sky is the limit for the Nifty to go up, there is a limit to a Put buyer’s loss which cannot go beyond the premium he has paid while buying the options contract.

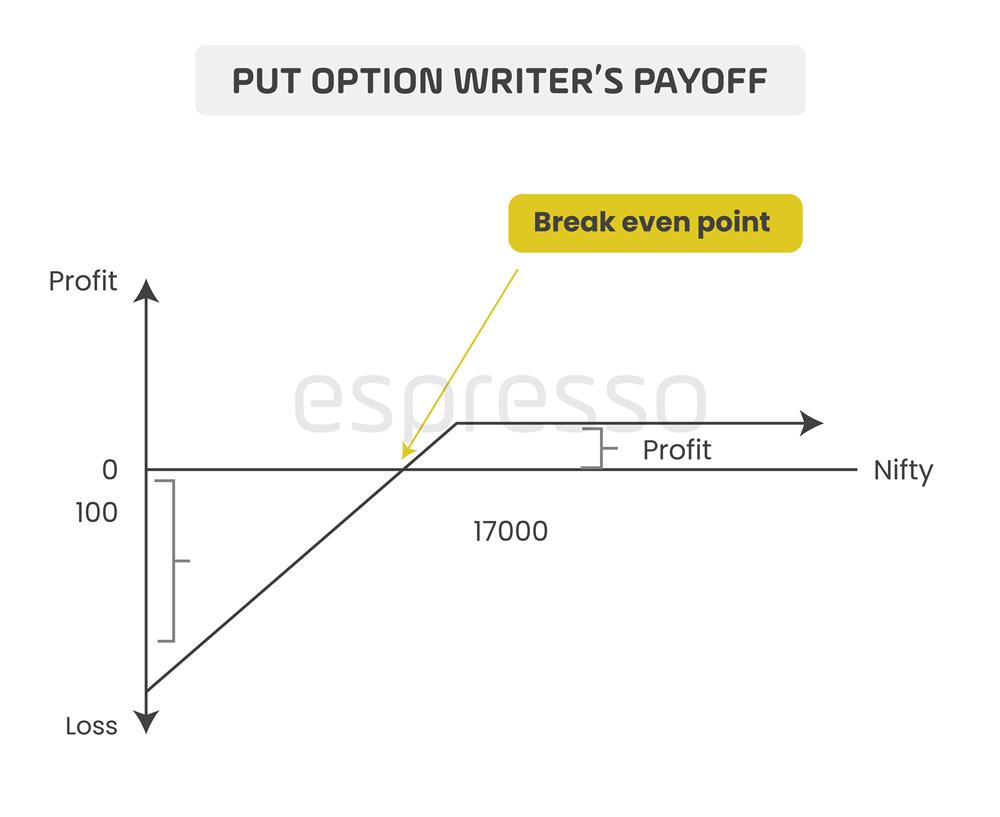

A Put Writer is the seller of a put option; he is the initiator of the transaction. Put Writers are usually seasoned market players with high net worth. For selling the Option, the Put Writer charges a premium which is his income. This premium is largely based on the time value and the risk perception in the market. In simple words, whatever is the Put Option Buyer’s profit/loss will be the Put Writer’s loss/profit.

A Put Writer is the seller of a put option; he is the initiator of the transaction. Put Writers are usually seasoned market players with high net worth. For selling the Option, the Put Writer charges a premium which is his income. This premium is largely based on the time value and the risk perception in the market. In simple words, whatever is the Put Option Buyer’s profit/loss will be the Put Writer’s loss/profit.

The above diagram clearly shows that there is a limit to the profit which a Put Writer can earn, while there is no limit on the loss that he may incur.

The profit/loss that both parties to the contract made on the option depend directly on the spot price of the underlying on the expiry day.

On expiration, if the spot price happens to be below the strike price, the buyer will exercise the option on the option writer. On the other hand, if the spot price of the underlying is more than the strike price on expiration, the buyer will let his option go un-exercised and the entire premium on the option will become the Writer’s profit.

The above diagram clearly depicts the Option Writer’s Profit/Loss zones. As Nifty starts falling in the Spot Market and slips below the strike price, the put option becomes ITM and the writer starts incurring losses. Thus, on expiration day, if Nifty closes below 17,000 in the spot market, the Put Writer will incur a loss as the Put buyer will exercise his option. The loss will be to the extent of the difference between the strike price and the Nifty closing price on expiration. It should be noted that the loss that the Put Option Writer may incur is limited to a maximum extent of the strike price as the lowest level Nifty can touch is zero.

Thus, the Put Option Writer’s loss will be unlimited within the limit of zero. In that sense, the Put Option Writer’s business is slightly safer than that of the Call Option Writer, where the risk of loss is unlimited.

Things to remember

- Put Options are bought by traders in a weak or falling market. Put options are preferred by the trader over Futures because the trader’s potential maximum losses are predefined, which makes his risk-reward profile much simpler.

- A Put Writer is the seller of a put option and is usually a seasoned market player with a high net worth. The Put Writer’s loss/profit is the Put Option Buyer’s profit/loss.

0

|

0

|

0

0