Watch

Watch Buying call options is the simplest way of trading in derivatives in the stock markets, not because returns are unlimited but because your losses are predetermined. Even such losses can be minimised and profits maximised through proper risk-reward analysis. Such analysis is made simple through payoff diagrams.

The profit/loss that the buyer of a call option makes depends on the spot price of the underlying stock. If on the expiry date, the spot price exceeds the strike price, the buyer will make a profit, and his profit will depend on how much higher the spot price is over the strike price.  On the other hand, if the spot price of the underlying is less than the strike price, the buyer will let his option expire un-exercised, and his loss, in this case, will be restricted to the premium he paid for buying the option.

On the other hand, if the spot price of the underlying is less than the strike price, the buyer will let his option expire un-exercised, and his loss, in this case, will be restricted to the premium he paid for buying the option.

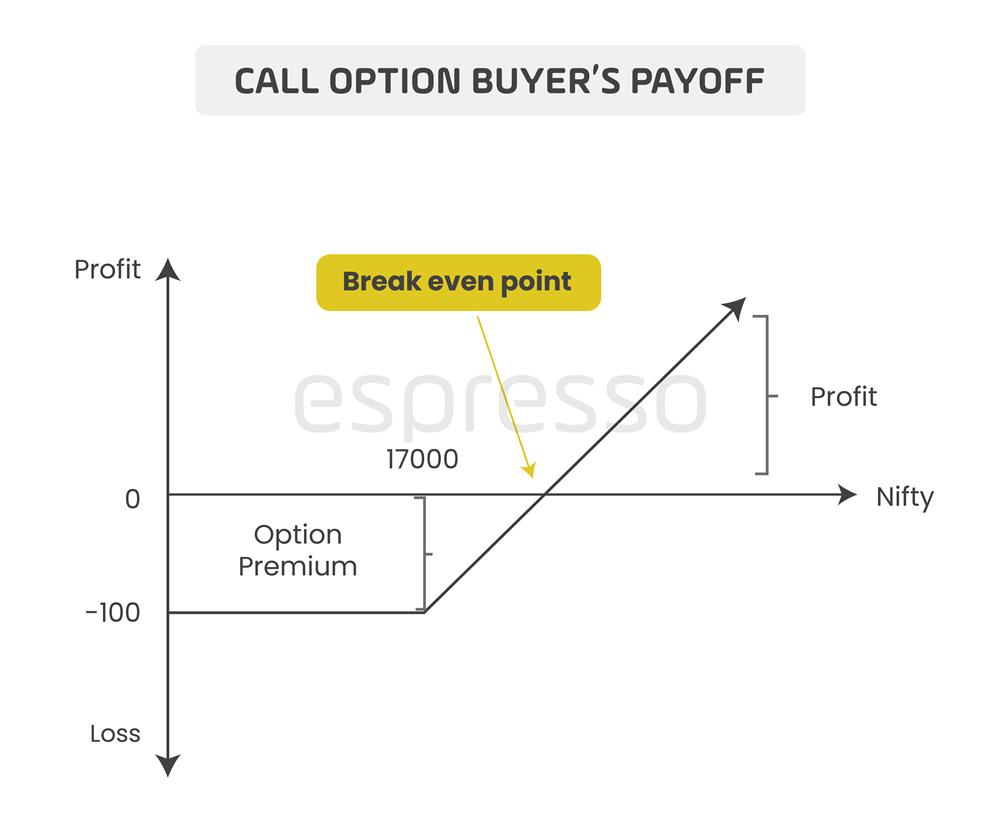

Suppose you buy a three-month Nifty call option at a strike price of 17,000 for a premium of, say Rs 100. Then your call option payoff diagram will appear, as shown above, clearly showing your profits/losses as a buyer of the call option. In the above diagram, the horizontal line indicates Nifty price movement while the vertical line indicates profit/loss made. As the Nifty moves beyond 17,000, your call option becomes In-The-Money (ITM). If on the expiry date, Nifty closes above your strike price of 17,000 (+option premium), you can exercise your option, which will bring in profit to the extent of the difference between the closing value of Nifty and the strike price. Anywhere below the breakeven point (price), the option will not be favourable to you and you will end up losing money on the option contract.  The diagram also shows that theoretically, profits possible on this option are unlimited. On the other hand, if Nifty closes below 17,000 on expiry day, you will incur a loss which, in any case, will not be more than the option premium you have paid.

The diagram also shows that theoretically, profits possible on this option are unlimited. On the other hand, if Nifty closes below 17,000 on expiry day, you will incur a loss which, in any case, will not be more than the option premium you have paid.

Based on the above example, your P&L table will appear as follows:

| On expiry Nifty closes at | CE buyer’s payoff |

| 16700 | -100 |

| 16800 | -100 |

| 16900 | -100 |

| 17000 | -100 |

| 17100 | 0 |

| 17200 | 100 |

| 17300 | 200 |

The above table is prepared based on the theoretical assumption that option premium and index price move in tandem (rupee to rupee), which may not be the case in reality. From the table, it is clear that strike price and option premium are the two important factors which determine your profit/loss. Thus, you, as a call option buyer, will be in the negative zone as long as the actual price is below the strike price (plus premium), will move to the neutral zone when the actual price reaches the strike price (plus premium), and will start making a profit when the actual price moves beyond the strike price (plus premium).

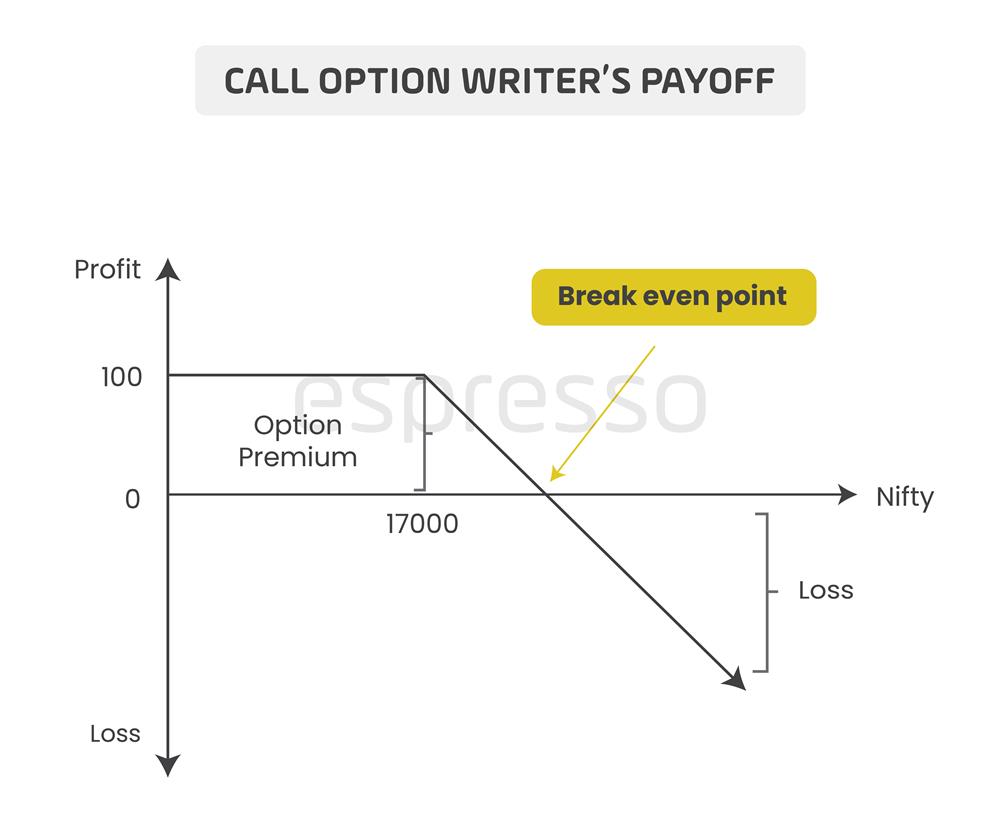

You can buy a call option only when somebody is willing to sell the same; they are the option sellers, also called option writers. They are the ones who initiate/create the transaction. Call writers charge a premium for selling calls. In simple terms, the call buyer’s profit is the call writer’s loss. A call buyer makes a profit when the spot price moves above the strike price. The call buyer, in such cases, makes a profit by exercising the option on the call writer. Thus, a call writer starts incurring losses once the spot price moves beyond the strike price. His loss will be directly related to the amount by which the spot price has moved beyond the strike price. On the other hand, if the spot price on expiry day is less than the strike price, it will be an ideal situation for the call writer as he will earn a profit on his sale. In such cases, the buyer would let his option expire un-exercised, thus allowing the writer to get the premium.

You can buy a call option only when somebody is willing to sell the same; they are the option sellers, also called option writers. They are the ones who initiate/create the transaction. Call writers charge a premium for selling calls. In simple terms, the call buyer’s profit is the call writer’s loss. A call buyer makes a profit when the spot price moves above the strike price. The call buyer, in such cases, makes a profit by exercising the option on the call writer. Thus, a call writer starts incurring losses once the spot price moves beyond the strike price. His loss will be directly related to the amount by which the spot price has moved beyond the strike price. On the other hand, if the spot price on expiry day is less than the strike price, it will be an ideal situation for the call writer as he will earn a profit on his sale. In such cases, the buyer would let his option expire un-exercised, thus allowing the writer to get the premium.

In the above example, the call writer will make a profit as long as the Nifty remains below 17,100. Once it moves above 17,100, he starts incurring losses, and his loss keeps increasing as Nifty goes up and up beyond 17,100. Theoretically, the option writer’s loss could be unlimited. And his profit will be limited to the extent of the premium charged.

Thus, while the call buyer will have scope for unlimited profit with limited loss, the call writer will face the risk of unlimited loss with limited profit/return. This makes the call writing business very risky, suitable only for those of high net worth and a deep understanding of the market. From this, it also follows that the higher the risk, the higher will be the option premium.

The call option buyer buys a call when he is sure of the stock price or index going up. Before taking the plunge, the call buyer makes a thorough risk-reward analysis. A long call option is the simplest way to benefit when your analysis says that the market will make an upward move, and it is the most common choice among first-time investors in options.

Things to remember

- When you buy a call option, your profit is limited, but your maximum loss, too, is predetermined by the premium paid. But profits can be maximised and losses minimised through proper risk-reward analysis. Such an analysis is made simple through pay-off diagrams.

- On the expiry date, if the spot price exceeds the strike price, the buyer will make a profit. If the spot price of the underlying is less than the strike price, the buyer will let his option expire un-exercised, restricting his loss to the premium he paid for buying the option.

- The call option buyer will be in the negative zone as long as the actual price is below the strike price (plus premium), move to the neutral zone when the actual price reaches the strike price (plus premium), and start making a profit when the actual price moves beyond the strike price (plus premium).

0

|

0

|

0

0