Watch

Watch In the last chapter, we talked about the key differences between price and value of a stock. But we have often heard analysts speak about stock valuations. So, are the terms value and valuation interchangeable? Let’s take a look.

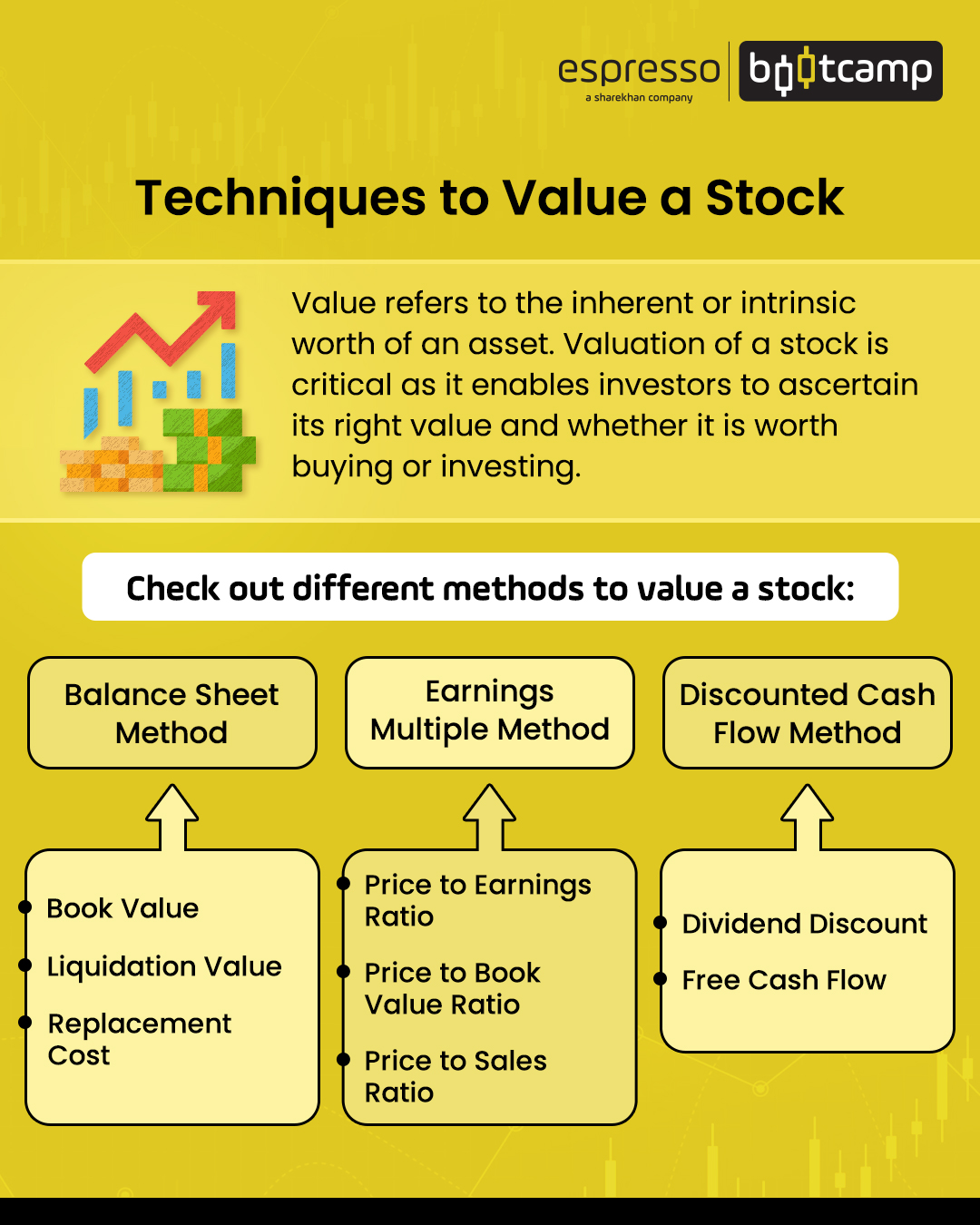

Value refers to the worth of an asset, while valuation is the process of arriving at the value.

While stocks, bonds, real estate, etc., are examples of assets, their price is quoted in the markets. Value refers to the inherent or intrinsic worth of an asset.

Valuation of an asset is critical as it enables buyers or investors to ascertain its right value and whether it is worth buying or investing.

To recall from the last chapter, the price could be higher or lower than the value of a product or asset. The buyer ends up with the raw deal of a bargain if the price is less than the value, and the seller loses out if the price is more than the value.

It is, therefore, necessary to undertake the exercise of valuation and to apply the right valuation method to be sure you have a fair deal. Though it isn’t quantifiable, some valuation methods help derive approximate values, taking into consideration relevant variables, to arrive at a value.

The need for valuation

The need for valuation arises because it is the starting point for price negotiation for buying or selling any asset. Valuation is undertaken by different stakeholders to fulfil their respective purpose.

- An investor may use various valuation methods to assess whether his long-term goals are achievable

- A business entity may use valuation techniques to assess another business entity that it seeks to buy

- Similarly, a business entity may use a different valuation method to assess if it should exit a business or the right value

- Peer comparison can be done using valuation methods to understand where a business entity stands vis-à-vis peers

- Corporate mergers and acquisitions depend a lot on the valuation of the companies and the valuation method applied

- Employee benefits like ESOPs can be assessed using specific valuation methods

- It is also done for regulatory and legal compliance

Valuation method or valuation techniques

We will discuss the three most popular valuation methods:

Discounted cash flow (DCF): This is a valuation method that uses future the projected free cash flows of a company and discounts it with an appropriate discount rate to arrive at the intrinsic value. Knowing how to use the DCF method, it is essential to understand the concepts of the time value of money (TVM), present value (PV) and future value (FV).

Time Value of Money (TVM): This valuation method is based on the concept that a sum of money in hand today is worth more than the sum of money that will be received in future. This is because money can be invested, and it grows if invested but depreciates if not.

Future value (FV): This is the value of money that will be received in future if invested at a certain rate of return. When we create a fixed deposit with a bank for a certain number of years, the interest is also reinvested, and the future value is more than the invested amount.

Formula: FV= PV X (1+r) ^n.

This is the formula of compound interest that we have learnt in school.

Present value (PV) implies money received in future is worth much lesser today.

Formula: PV= FV X 1/(1+r) ^n

Weighted average cost of capital (WACC) is the discount rate used which comprises the average cost of every source of capital, including equity and debt weighted by their proportion.

Terminal value (TV) is an assumption that the cash flows will grow at a stable rate after the forecast or projected period. The terminal value will also have to be discounted. The formula is different in this case.

PV of terminal year cash flow = Terminal year cash flow X (1+ terminal growth rate)/ (WACC – terminal growth rate).

Free cash flow is the cash flow from the operations of a company after deducting capital expenditure.

Here's an example to drive home the point:

The cash flow of a company for Year-1 is Rs 1,000 crore which is expected to grow by 10% every year. The WACC or discount rate is 12%. The terminal period is five years. From Year-6, the cash flow is expected to grow by 3% perpetually. The debt on the balance sheet is Rs 10570 crore and cash and cash equivalents are Rs 1750 crore. The outstanding equity shares are Rs 75 crore.

Let us calculate the intrinsic value from the available data:

| Years | Growth (%) | Free cash flow (Rs. Cr) | A discount factor of 12% | Discounted cash flow (Rs. Cr) or PV |

|

Year-1 |

10% |

1000 |

0.893 |

893.0 |

|

Year-2 |

10% |

1100 |

0.797 |

876.7 |

|

Year-3 |

10% |

1210 |

0.712 |

861.5 |

|

Year-4 |

10% |

1331 |

0.636 |

846.5 |

|

Year-5 (terminal year) |

10% |

1464.1 |

0.567 |

830.1 |

|

NPV of the projected period |

4307.9 |

|||

|

|

||||

|

Terminal value |

|

|

|

|

|

Terminal year cash flow |

1464.1 |

|

|

|

|

Terminal period growth rate |

3% |

Total NPV (4307.9 + 16755.81) |

21063.69 |

|

|

Discount rate |

12% |

|||

|

PV of terminal cash flow |

16755.81 |

|

|

|

To calculate enterprise value, we have to add net debt, i.e., total borrowings minus cash and cash equivalents.

| Total NPV | 21063.69 |

|

Add: Borrowings |

10570 |

|

Less; Cash & cash equivalents |

1750 |

|

Enterprise value (EV) |

29883.69 |

|

Outstanding equity shares |

75 |

|

Intrinsic value per share (EV/equity shares) |

398.45 |

Multiplier method

Also known as the market valuation method, as it uses market price, the multiplier method is one of the most popular methods to arrive at the value of the business. However, one has to understand that this method must be applied to companies in similar businesses.

In this approach, a set of companies are identified, and their multiples are arrived at and the average multiple is computed. This multiple is used to compute the value of the business. A multiple is nothing but a ratio where either the market price or enterprise value is divided by an element of the profit and loss account, balance sheet or cash flow statement like sales, EBIDTA or EPS.

| Name | P Rs. | Mar Cap Rs Cr | EPS 12M Rs. | P/E | Ind PE | P/ BV | EV / EBITDA | EV / Sales | P/ OCF |

|

Eicher Motors |

2631.5 |

71937.73 |

58.26 |

45.17 |

33.64 |

6.24 |

26.78 |

6.73 |

41.99 |

|

Hero Motocorp |

2294.25 |

45855.7 |

129.46 |

17.73 |

33.64 |

2.92 |

11.06 |

3.82 |

11.15 |

|

TVS Motor Co. |

645.6 |

30677.11 |

16.62 |

38.02 |

33.64 |

7.64 |

14.15 |

3.49 |

26.64 |

|

Wardwizard Inno. |

72.6 |

1878.63 |

0.23 |

318.95 |

33.64 |

57.99 |

187.56 |

820.96 |

47607.45 |

|

P= Price, PE-Price to EPS, Ind PE= Industry PE, BV= Book value per share, EV= Enterprise value, OCF= Operating cash flows |

|||||||||

Asset-based valuation method

This is the simplest type of valuation method as it considers only the assets and liabilities of a company to arrive at its intrinsic value. This method is used for companies having a large portion of tangible assets in their books.

Companies in sectors such as aviation and infrastructure have a larger component of tangible assets in their books. There are a few variants of this method:

Liquidation value is the book value arrived at if all the assets and liabilities are liquidated, except intangibles.

Going concern variant includes intangibles also as a part of net assets, thereby realising a higher book value.

| Particulars | Net Asset Value (Rs Cr) |

Revalued Net Asset Value (Rs Cr) |

|

Tangible Assets |

5500 |

7500 |

|

Intangible Assets (patents, software etc. |

700 |

700 |

|

Goodwill |

1200 |

|

|

Non-Current Investments |

200 |

200 |

|

Current Investments |

400 |

400 |

|

Other assets |

600 |

600 |

|

Total Assets |

8600 |

9400 |

|

Long-Term Borrowings |

4000 |

4000 |

|

Short-term liabilities |

2500 |

2500 |

|

Liabilities |

6500 |

6500 |

|

Book value |

2100 |

2900 |

|

Equity shares (Nos) |

20 |

20 |

|

Book value |

105 |

145 |

Points to remember

- Valuation is the starting point for price negotiation for buying or selling any stock or asset

- Valuation method or valuation techniques are used by different stakeholders to fulfil their respective purpose

- It is important for traders and investors to have the knowledge of the right valuation method or valuation techniques to make wise trades and investments

0

|

0

|

0

0