Watch

Watch In general, mark-to-market is a method which is used to determine the fair value of an asset or liability based on the present market condition. In some segments of the financial markets trading, such as futures, the profits and losses on trade are computed on an M2M basis.

In simple terms, the profits and losses of a futures position taken up by a trader are computed and settled regularly throughout the life cycle of the contract. In the Indian markets, the M2M profits and losses are calculated on a daily basis as the difference between the previous and current day’s settlement price. These losses are paid out and profits are received into the trading account of the member at the end of each trading day.

Thus, M2M is the settlement of the daily profits and losses based on the changes in the market value of the stock. In futures contracts, when the underlying stock’s value falls in a day, the seller of the contract gets money from the buyer. When the price rises, the buyer collects money from the seller of the contract. This settlement is done daily and is called MTM.

Futures, being a leveraged financial product, are traded by members through margins which are kept as “deposits of good faith” in their trading accounts as cash. In other words, when entering a futures trade, the trading member must maintain a certain initial margin in their account, which represents only a small fraction of the overall value of the contract.

How does MTM work?

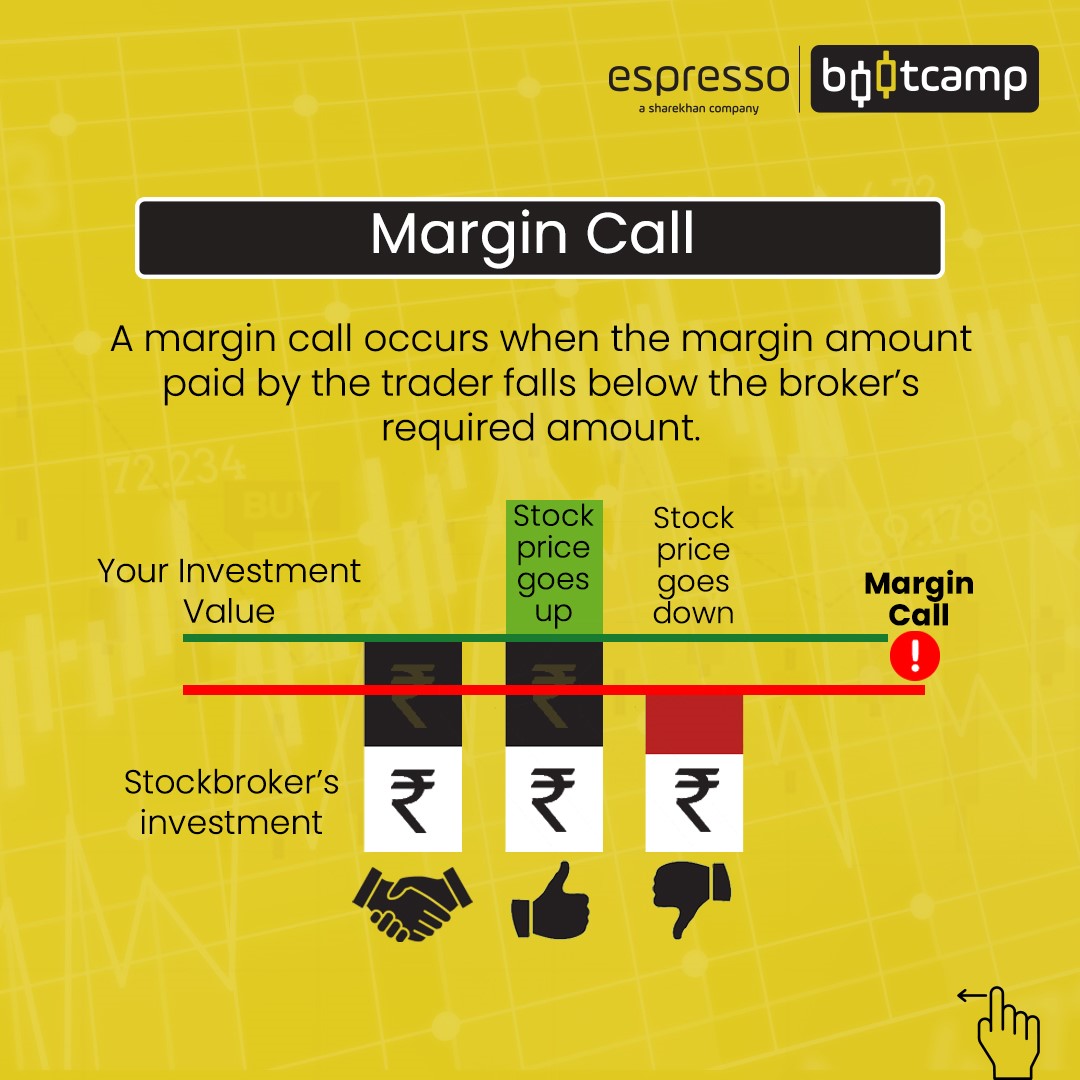

From the day of the entry into the trade, as the markets fluctuate, profits are credited, and losses are debited to the account of the trader on a daily basis as per the M2M settlement mechanism. As a result, the value of the margin kept in the account of the trading member varies daily. If the market moves against the direction in which the trader has taken a position, the initial margin starts to deplete. As the value of this initial margin falls below the maintenance margin, the trading member receives a margin call.

The underlying mechanism can be better understood through the following example:

Suppose, Trader A buys a futures contract of HDFC Bank on Monday, which is currently trading at Rs 1,460 because he has a bullish inclination about the stock's price. Each futures contract represents 550 shares of HDFC Bank. For purchasing this contract, assume that Trader A has to provide an initial margin of Rs 1,45,000. Further, assume that the maintenance margin is Rs 1,30,000.

Finally, assume that the futures contract price moves to Rs 1,470 on Tuesday, come down to Rs 1,450 on Wednesday and finally settles at Rs 1,420 on Thursday. Due to this movement, the M2M mechanism will have the following impact on the account of Trader

| Day | Futures Price | P&L per share | Lot Size | Total P&L | Margin at Beginning | Margin at End |

| Monday | 1,460 | - | 550 | - | 1,45,000 | 1,45,000 |

| Tuesday | 1,470 | +10 | 550 | +5,500 | 1,45,000 | 1,50,500 |

| Wednesday | 1,450 | +20 | 550 | -11,000 | 1,50,500 | 1,39,500 |

| Thursday | 1,420 | +30 | 550 | -16,500 | 1,39,500 | 1,23,000 |

As presented in the ‘Margin at End’ column of the above table, the margin amount in Trader A’s account will keep fluctuating on a daily basis. Further, Trader A will receive a margin call on Thursday because the margin in his account has fallen below the maintenance margin of Rs. 1,30,000 due to the M2M loss on that day.

Points to remember:

- Mark-to-market can help a trader know about their profit or loss in futures and options trades.

- If the margin in a trader’s account falls below the minimum level, the broker will initiate a margin call.

0

|

0

|

0

0