Watch

Watch Imagine that Maruti Suzuki has got an order from the government to supply 500 cars in two months. The company is planning to start production in two months. It calls its supplier, CarSteel Ltd, and asks for a price quote for steel.

Now, Maruti knows that there is a COVID-19 outbreak in some cities across China, and the government has ordered a strict lockdown. It also feels that as the wave continues, some large steel factories in China might be forced to halt production, causing a spike in steel prices.

If Maruti does not take preventive measures, its profit margins in the coming quarter might be impacted negatively.

In such a scenario, Maruti Suzuki can negotiate a contract with CarSteel Ltd, their long-term supplier. As part of this agreement, Maruti agrees that it will buy 700 tonnes of steel at a price of steel at USD 1,200 per tonne one month later.

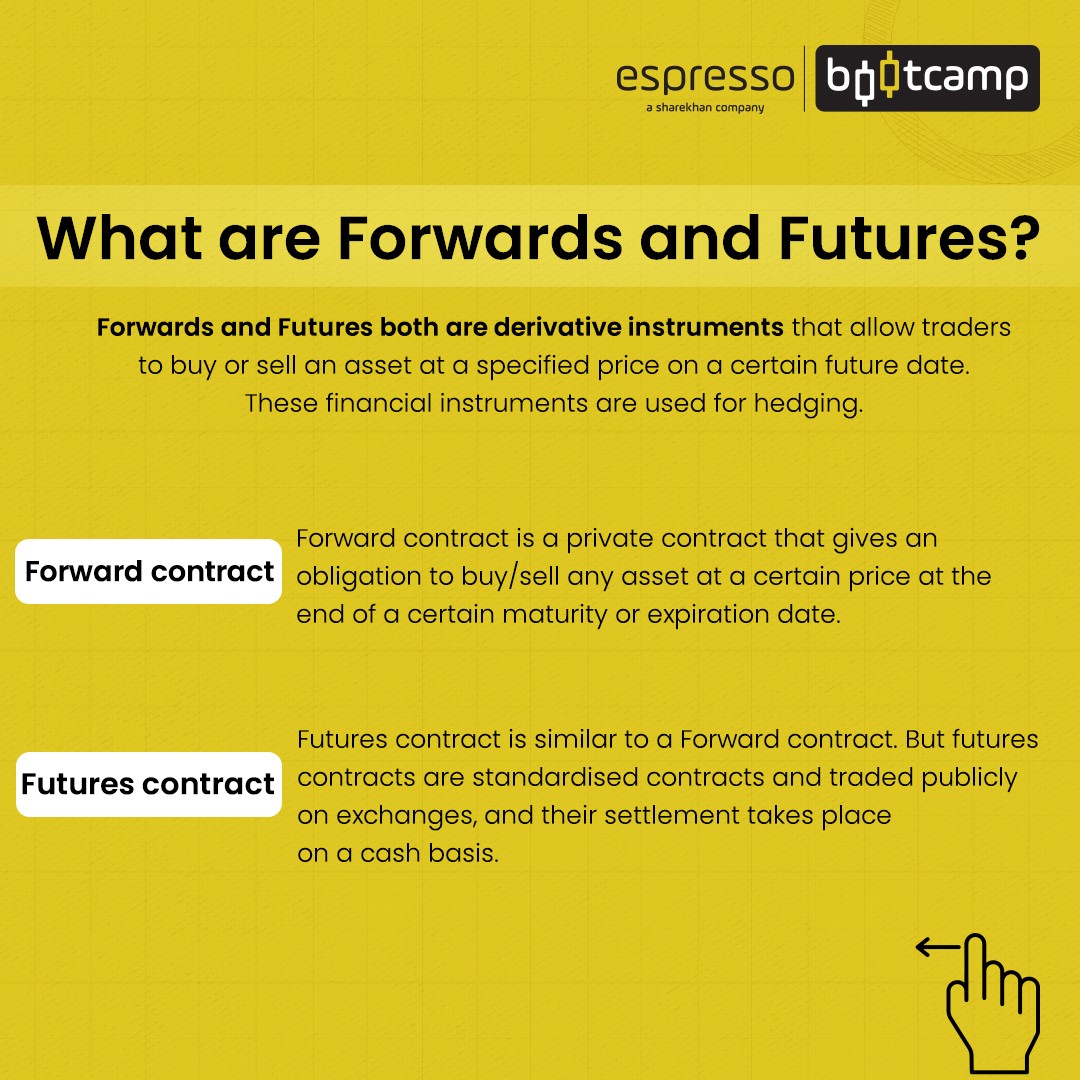

Such an agreement is called a forward contract, and it is typically binding on both parties. Now, consider the following possibilities:

Scenario 1

The COVID-19 outbreak in China spreads rapidly, and prices of steel have risen to USD 1,500 per tonne one month later. In this case, had Maruti Suzuki not entered into the forward agreement with CarSteel Ltd., it would have had to pay USD 1,500 x 700 tonnes = USD 1,050,000.

However, since Maruti Suzuki has the forward contract in place, it needs to pay only USD 1,200 per tonne, irrespective of the current market price. As a result, the company ends up paying only USD 840,000 for 700 tonnes at USD 1,200 per tonne. In this scenario, Maruti Suzuki was saved.

Scenario 2

The lockdown measures taken by the government are successful at reducing the number of infections and the Chinese steel factories continue to function as usual. This leads to global steel prices falling mildly to USD 1,150 per tonne a month from today.

Now, Maruti Suzuki still has to pay USD 1,200 per tonne for the 700 tonnes of steel, leading to a total expense of USD 1,200 * 700 tonnes = USD 840,000 for the company. In case they had not entered into the forward contract, Maruti Suzuki would have been able to procure the steel at the current market price, i.e. USD 1,150 per tonne. This would lead to a cost of USD 1,150 * 700 tonnes = USD 805,000. In this scenario, Maruti Suzuki lost.

Now, a large corporation like Maruti is not interested in trying to earn additional profit by speculating on the prices of steel. It is interested in keeping its earnings predictable in the near term, even if it means fixing its purchase price could result in a potential loss, such as what it saw in scenario 2.

Put simply, Maruti is interested in protecting itself – it wants to hedge itself -- against fluctuations in raw material price. Its supplier likely had a similar goal: to have predictability in its revenue. This is why it agreed to sign the contract.

And for a party interested in such hedging, a forward contract is the perfect tool to do it.

Futures vs Forward contract

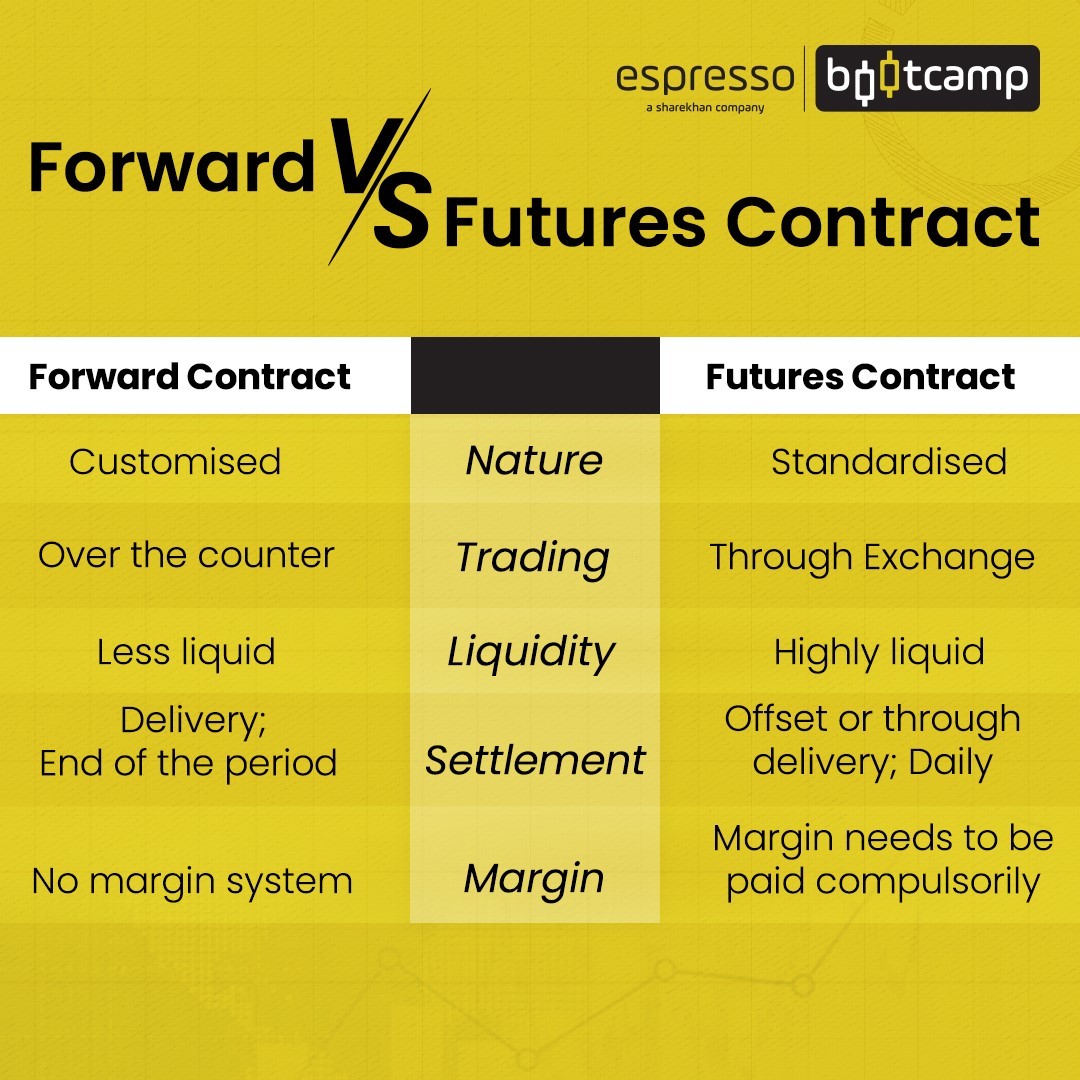

Similar to forward contracts, some futures contracts allow traders to buy or sell an asset at a specified price on a certain date. A key difference between forward and future contract is that futures are traded publicly on exchanges, while forwards are private contracts. Futures are standardised contracts, and their settlement occurs on a cash basis.

Futures contracts are mostly used for hedging and speculating. Traders hedge their positions through futures with an aim to reduce the chances of any loss in case of any unfavourable price movement of the underlying asset. Futures are also used by companies and traders to speculate in an attempt to gain profits.

For instance, if you think the share price of Reliance Industries will rise, you can buy a single lot of futures contract at its current price (say Rs 2,500), which contains a fixed number of shares (say: 100) and with a fixed delivery date (say the end of this month).

Unlike the forward contract, the seller is not necessarily required to send you 100 shares of Reliance Industries at the agreed price of Rs 2,500. In fact, if the price goes up to Rs 2,600 tomorrow, you can sell your contract to someone else and make a profit of Rs 10,000 (because each lot contains 100 shares).

History of futures trading in India

Futures are traded on exchanges just like stocks and bonds, with the distinction of the mark-to-market settlement process. In India, futures for stock indices, equities, global indices, currency pairs, bonds and commodities are traded on the major exchanges: National Stock Exchange (NSE) and the Bombay Stock Exchange (BSE). Commodity futures are also traded on exchanges like the Multi Commodity Exchange of India (MCX) and the National Commodity and Derivatives Exchange (NCDEX).

BSE and NSE started futures trading a few months apart in the year 2000. Ever since their introduction in India, the market for futures has grown exponentially, with often over 5 lakh index futures contracts (valued at a little over Rs 28,000 crore) trading hands on the NSE. The relative value of the derivatives contracts traded on the BSE is significantly lower than NSE.

Some of the important market participants in the futures segment in India are hedgers and speculators. While hedgers seek to use futures contracts to safeguard themselves from volatility in financial assets, speculators try and predict the directions of market movements and earn profits through such movements.

In India, the Forward Markets Commission (FMC) was established in 1953 as a regulatory body for the commodity futures market. It monitors and regulates the commodity futures trading in the country and works towards ensuring financial and market integrity.

To strengthen the regulation of the commodity futures market, the Forward Markets Commission was merged with the Securities and Exchange Board of India (SEBI) on 28 September 2015.

Points to remember:

- Forward contracts are great tools for hedging against price fluctuations.

- The key difference between a future and forward contract is that futures are traded publicly.

0

|

0

|

0

0